There are fresh hints that the Thrift Savings Plan is considering whether to offer investment advice to its 4.7 million members.

Buried in a just-released report on the White House’s 2015 Conference on Aging is mention that the “Federal Retirement Thrift Investment Board is formally considering whether to provide more personalized investment advice.”

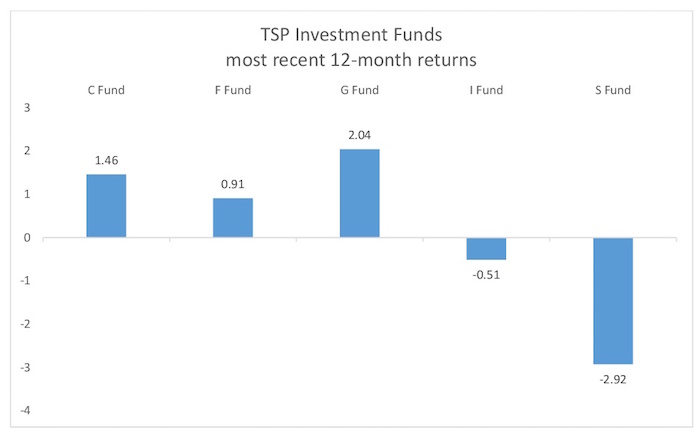

TSP is the nation’s largest 401(k)-type retirement plan with $454 billion in assets, but members currently receive very little help in choosing how much to invest and how to allocate their contributions among TSP’s various funds.

Currently, the closest TSP comes to giving advice is its Lifecycle funds, which “use professionally determined investment mixes that are tailored to meet investment objectives based on various time horizons. The objective is to strike an optimal balance between the expected risk and return associated with each fund,” according to the TSP web site.

This past July, The Washington Post reported that the FRTIB Board received a report that “41 percent of investors who left the government in 2012 transferred their money out of TSP within a year, rather than leaving it in place as is allowed.” There are indications that the percentage has increased to 55 percent.

The Board feels that not providing investment advice is one of the reasons retirees move their money out of TSP into other retirement vehicles, such as an IRA. A separate Withdrawal Survey Report presented to the FRTIB Board in 2014 suggested that 15 to 23 percent of survey respondents who withdrew their savings had a desire for a financial adviser or financial advice.

One consideration is whether to charge for such professional advice. The advantage of charging a fee for investment advice is that it would be paid only by TSP members interested in the service. The downside is that fewer members would want advice if they had to pay additionally for it.

Alternatively, the TSP could offer the advice free to all members, but then it would have to absorb those additional expenses, which would raise the costs for all participants, even those who would not be interested in taking advantage of the service. As TSP prides itself in its low administrative overhead, any additional cost would lower investment returns by an unknown amount depending on the cost of the service.

Determining the cost of advice would be dependent on how personalized TSP chooses to make its service. Do a Google search on investment advice, and you will find a host of private sector advisers ranging from advisers willing to meet one-on-one with participants to develop personalized investment strategies to investment apps where you input your information to receive results based on algorithms. The more personalized the service, the higher the expected cost.

In a FedSmith survey published in September, the majority of survey respondents who participate in the TSP indicated that they do not use a financial adviser when making their investment decisions. Ninety percent of respondents said they do not currently use a financial planner to assist with setting up TSP investments. Only five percent of respondents said they subscribe to a service that advises when to buy or sell the various TSP funds.

All this discussion comes at the same time that the Department of Labor is moving to update its rules on investment advisers and has led to lawmakers introducing legislation to stop the DOL proposal and substitute less stringent requirements fearing that the new rule will make advice too costly for individuals with modest retirement accounts.

The FRTIB’s interest in advice is just one of the approaches underway to increase and sustain members’ involvement in the TSP. This year, the Board will be asking Congress for permission to provide more flexibility in how members may make withdrawals, and it continues to show an interest in offering mutual funds as investment options.

With 2016 being a Presidential election year, TSP members will have to wait to see what changes may await them based on Congress’s level of interest in these topics.