When the Thrift Savings Plan (TSP) introduced its mutual fund window, the idea was straightforward: give federal employees access to thousands of additional investment options and participation would follow.

It hasn’t.

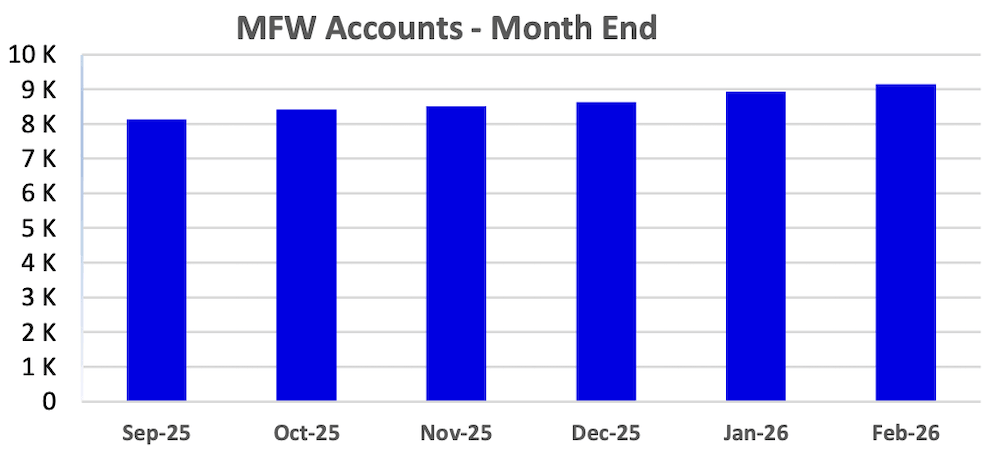

Several years after its launch, the mutual fund window remains one of the least-used features in the TSP. Despite offering access to more than 4,000 mutual funds, a little over 9,000 participants had funded accounts as of the end of February 2026, according to the Federal Retirement Thrift Investment Board. Out of more than 7 million participants, that is far less than one-tenth of one percent.

In a system known for its simplicity and low costs, the mutual fund window has quietly become a niche option.

On paper, the mutual fund window addressed a long-standing request. Some participants wanted access to investments beyond the familiar core lineup of the C, S, I, F, and G Funds. The new feature promised flexibility, opening the door to sector funds, actively managed strategies, and more specialized investment approaches.

But in practice, most participants never felt the need to use it. The core TSP funds already provide broad exposure to the major segments of the global markets. For many federal employees, that has proven to be enough.

The Problem of Cost

Cost is one of the clearest explanations for the low adoption rate.

The TSP has built its reputation on being one of the lowest-cost retirement plans in the country. Its core funds operate with extremely low expense ratios, which quietly but powerfully support long-term returns.

The mutual fund window changes that equation. Participants must pay a $150 annual administrative fee, along with additional trading costs and the internal expenses of the funds themselves. For investors accustomed to paying very little, this represents a meaningful increase.

Complexity vs. Simplicity

Another important factor is complexity.

The TSP’s success has always been tied to its simplicity. Participants are not required to sort through thousands of investment choices. Instead, they can build a diversified portfolio using a small number of broad funds or rely on Lifecycle (L) Funds to handle allocation automatically.

The mutual fund window introduces a very different experience. Suddenly, participants are faced with thousands of options, each with its own strategy, cost structure, and risk profile.

That level of choice can create unintended consequences. Investors may feel pressure to time the market, chase recent performance, or construct overly complicated portfolios. In many cases, more options do not lead to better decisions but rather to more opportunities for error.

The 25 Percent Limitation

The structure of the mutual fund window also limits its usefulness.

Participants can invest only up to 25 percent of their TSP balance in the window, with the remaining 75 percent required to stay in the core funds. This cap makes it difficult to fully implement a strategy centered on outside mutual funds.

For many participants, that restriction reduces the appeal of the feature. If the majority of assets must remain in the core TSP anyway, the incentive to add complexity and cost for a limited portion of the portfolio becomes less compelling.

The low participation rate raises a broader question about whether the mutual fund window was ever necessary for most investors.

The existing TSP structure already allows participants to achieve broad diversification across stocks and bonds at very low cost. A simple allocation using the core funds, or a single Lifecycle Fund aligned with a retirement date, can form a highly effective long-term strategy.

As of the end of 2025, nearly 195,000 TSP participants had balances of $1 million or more.

Who May Benefit?

While adoption has been minimal, the mutual fund window is not without purpose.

It may appeal to some experienced investors who want access to specific strategies not available within the TSP. This could include targeted sector exposure or particular active management approaches. For those individuals, the additional flexibility may justify the higher costs and added complexity.

Even so, many participants may find that similar flexibility can be achieved outside the TSP, particularly after separating from federal service and rolling assets into an IRA.

What We Learned

The mutual fund window was introduced to expand choice within the TSP. What it has revealed instead is that most federal employees do not need more choices. They need reliable, cost-effective outcomes.

With fewer than 1 in 1,000 participants using the feature, the message is clear. Simplicity, low costs, and disciplined investing continue to drive retirement success. For the vast majority of TSP participants, the core funds are not a limitation. They are a strength.

Comments