I get it. You don’t want a mortgage in retirement, but taking a large TSP withdrawal to pay off the mortgage is probably not the best solution, at least not if you care about how much you pay in taxes.

Good Intentions

I think the famous saying goes something like, “The road to hell is paved with good intentions,” and that applies to finance more than you know.

One of the most common times that people get themselves into trouble is when they are trying to do something good/proactive without understanding all the details. Paying off your mortgage early is a great thing but how you do it makes a massive difference.

The BIG Problem

This is the problem in a nutshell: Whenever you take a large traditional TSP withdrawal, it is all added to your taxable income which often puts you in a higher tax bracket, and the higher tax bracket means you’ll probably need to withdraw more gross to be left with the net amount you need.

Example

Let’s say you are married and your normal income is $100k/year in retirement and you have $150k left to go on your mortgage with $800k in your Thrift Savings Plan (TSP).

Your mortgage payment is $1,800/month and you’d love to knock that all out at one time. You figure you have plenty in the TSP to cover it so you request a $150k withdrawal from your traditional TSP.

You are surprised, however, when TSP only sends you $120k and sends $30k directly to the IRS for taxes. You realize your mistake and request another $37.5k to be left with the needed $30k net after taxes.

So in total, you had to withdraw $187.5k to be left with $150k net to pay off the mortgage.

Tax Bracket Destruction

And what does this withdrawal do to your tax bracket?

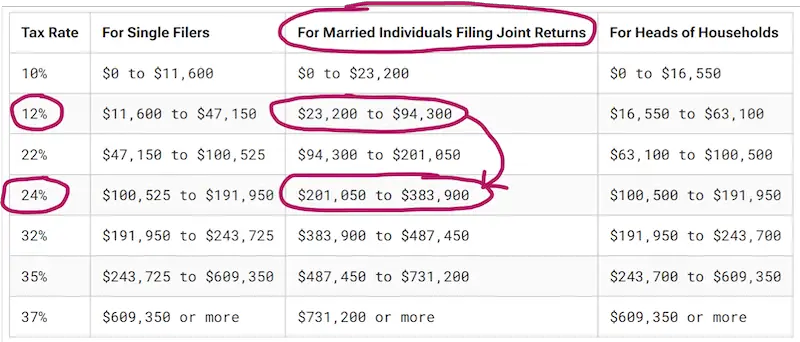

With an income of about $100k as a married person, you’d have a taxable income of about $70k after using the standard deduction of $29,200 (2024) which would put you in the 12% tax bracket as this chart shows.

| Tax Rate | For Single Filers | For Married Individuals Filing Joint Returns | For Heads of Households |

|---|---|---|---|

| 10% | $0 to $11,600 | $0 to $23,200 | $0 to $16,550 |

| 12% | $11,600 to $47,150 | $23,200 to $94,300 | $16,550 to $63,100 |

| 22% | $47,150 to $100,525 | $94,300 to $201,050 | $63,100 to $100,500 |

| 24% | $100,525 to $191,950 | $201,050 to $383,900 | $100,500 to $191,950 |

| 32% | $191,950 to $243,725 | $383,900 to $487,450 | $191,950 to $243,700 |

| 35% | $243,725 to $609,350 | $487,450 to $731,200 | $243,700 to $609,350 |

| 37% | $609,350 or more | $731,200 or more | $609,350 or more |

However, an additional $187.5k in taxable income would put you into the 24% bracket with a total taxable income of about $257.5k. See chart:

Medicare Nightmare

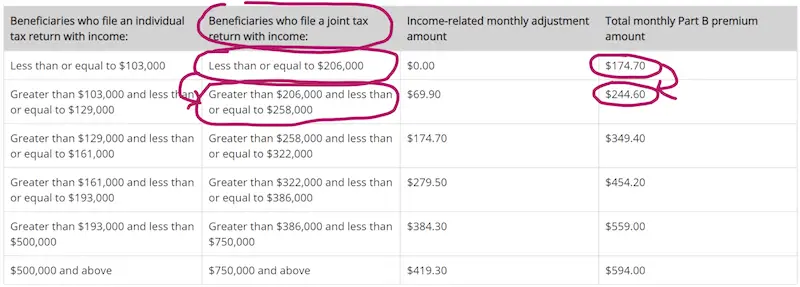

If jumping tax brackets wasn’t bad enough, this withdrawal would also affect your Medicare Part B premiums if you were 65+ years old.

Medicare Part B premiums are based on income. The more you make the more you pay.

This chart shows that you would pay about an extra $838.80/year ($69.90/month) per person because of that large withdrawal.

How Do You Make It Work?

But after all that, if you are still determined to get your mortgage paid off early, there is a better way.

The above tax problems were caused because of the large spike in income in a single tax year, but if we split up the withdrawals over multiple tax years, the tax impact would be much smaller.

For example, instead of withdrawing the entire needed amount in one year, you make the withdrawals in four pieces over four years. This way you minimize the tax implications.

Ideal Plan

The ideal plan would be to have the mortgage paid off by retirement so you don’t have to deal with any of these issues.

If you are early/mid-career then this may be reasonable to do. If you are late in your career then simply do the best you can with the time you have left.

Note: The higher your interest rate the more worried I’d be about paying off the mortgage early.

Final Thoughts

I am a huge fan of not having a mortgage in retirement. It lowers your expenses and makes your retirement income go further. It also just feels good to not have that large debt looming over you.

But with everything, you need to understand the ramifications of all your decisions before you pull the trigger on anything.