Federal employees are in a unique situation. The structure of FERS benefits allows for a good idea of when you may be able to retire. That consistency is not something other workers usually have, and it can be used as an advantage in planning this type of strategy.

Now I will say this, paying down a mortgage early is one of the more polarizing topics in personal finance. There is no shortage of opinions, based on emotional or analytical thinking, but the right answer comes down to your thoughts and what your finances look like.

Unsure how you feel about it? Ask yourself this question: Do you want to have a mortgage when you sign your retirement paperwork?

I tend to answer no, but I also don’t like the idea of leaving money on the table in other places.

Then I go back to thinking about some of the happiest retirees I know. They are the ones living without a mortgage. No debt, less stress and anxiety, lower expenses, and more flexibility.

In this post, I want to address the following topics:

- The benefits of this strategy

- Where it works well

- What to avoid

- How to make it happen

Make sure to check out the video I posted with additional context and examples for the discussion.

Does it Make Sense?

First, are you on track for retirement? You should be able to answer “yes” to this question to move forward confidently with a strategy to pay down your mortgage early. This means looking at the numbers.

How are your Federal Employees Retirement System (FERS) basic annuity and Social Security estimates looking? These are easy enough to find from your agency and at SSA.gov. Pull those numbers and consider how long you are planning to continue working.

Including your Thrift Savings Plan (TSP) account, how much are your investments worth? How much are you currently contributing and what are the projections looking like at retirement age?

Unsure how this translates? We can use the 4% rule to ballpark the income potential from your investments:

- Portfolio Value x 4% = Projected Income

- Income need x 25 = Portfolio Goal

Add it all up and compare it with your income goal. Are you on track? If you need to make up ground, that’s where you should focus right now. Remember, there isn’t an alternative funding source for retirement other than the work we put in.

Ranking or prioritizing your cash flow is also helpful. Cash flow is just a fancy word here for how we direct our resources or where our money goes.

For example, a priority order of cash flow might look like this:

- Emergency Cash Savings

- High-Interest Debt

- Retirement Savings

- Education Planning

- Other major goals [including mortgage paydown]

If you are on track and contributing enough for retirement, it’s time to think about some of the other goals you have. Do you want or need to fund education for your kids? Do you want to buy a vacation home or invest in real estate properties? Consider things that are part of your longer-term vision and prioritize them in order of importance. Just don’t take your foot off the gas on your retirement planning.

I could talk cash flow all day, but I might lose you. We’re here to talk about whether it makes sense to pay a mortgage down by retirement age.

Last question here: How much are you currently saving and how much additional cash flow do you think you might be able to put toward your goals in the future?

What Does Your Current Mortgage Look Like?

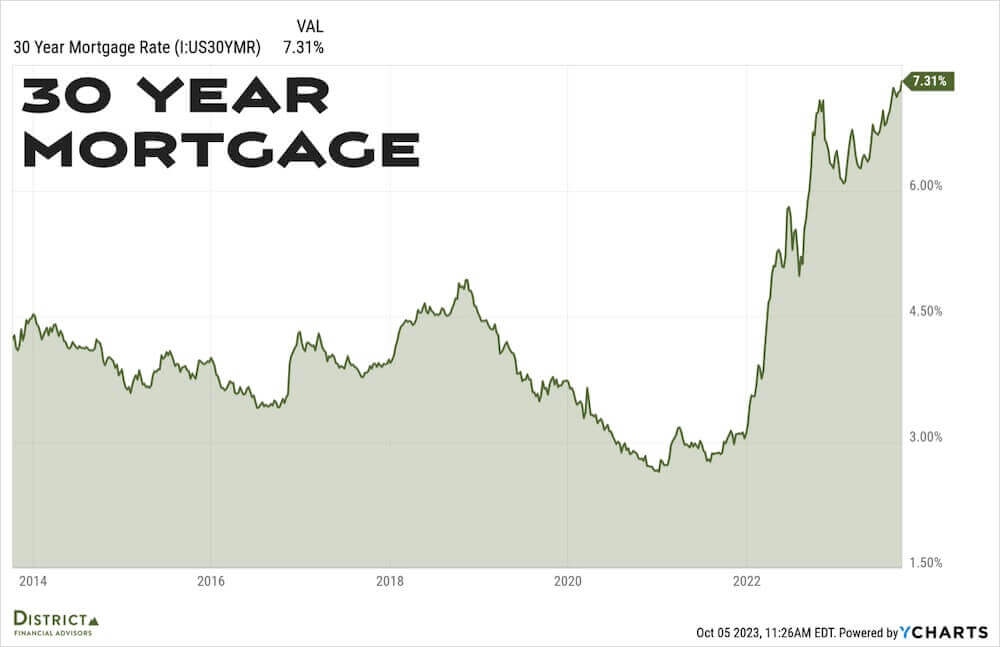

Mortgage rates are always interesting to look at in this conversation, especially as rates have risen dramatically in the past 2 years.

In the minds of many people, those previously low mortgage interest rates made the decision to not pay down a mortgage easier, but even if you are lucky enough to have a low mortgage rate locked in this strategy can work.

Rates are likely to stay higher for longer with what’s happening in the economy and country, and that is a consideration going forward but it’s not the only deciding factor.

A popular strategy for many people is to make one extra mortgage payment each year to chip away at the principal balance of the loan.

Let’s take a quick look at making that one extra payment per year on two 30-year fixed mortgages, each with a $650,000 principal balance but with different interest rates. In this example, we’ll divide the monthly principal and interest payments by 12 and add that amount to our payment each month to equal our one extra payment per year:

@4% – P&I payment $3,103.20, extra $258.58 per month (1/12) = 26 year payoff

@7% – P&I payment $4,324.47, extra $360.37 per month (1/12) = 24 year payoff

We can see both scenarios shave significant time off the term.

Interest rates play a role in several ways – required monthly payments, cumulative interest –paying more principal to match that higher monthly payment also impacts how fast the paydown happens.

It’s tempting to compare a payoff strategy of a lower interest rate mortgage to buying an investment with higher expected returns like stocks – going after a higher return than what you are paying in mortgage interest expense.

However, it’s not a fair comparison because when you’re paying down your mortgage, it’s a guaranteed rate of return in saved interest. We know stocks are far from guaranteed. There’s no telling what future performance will be.

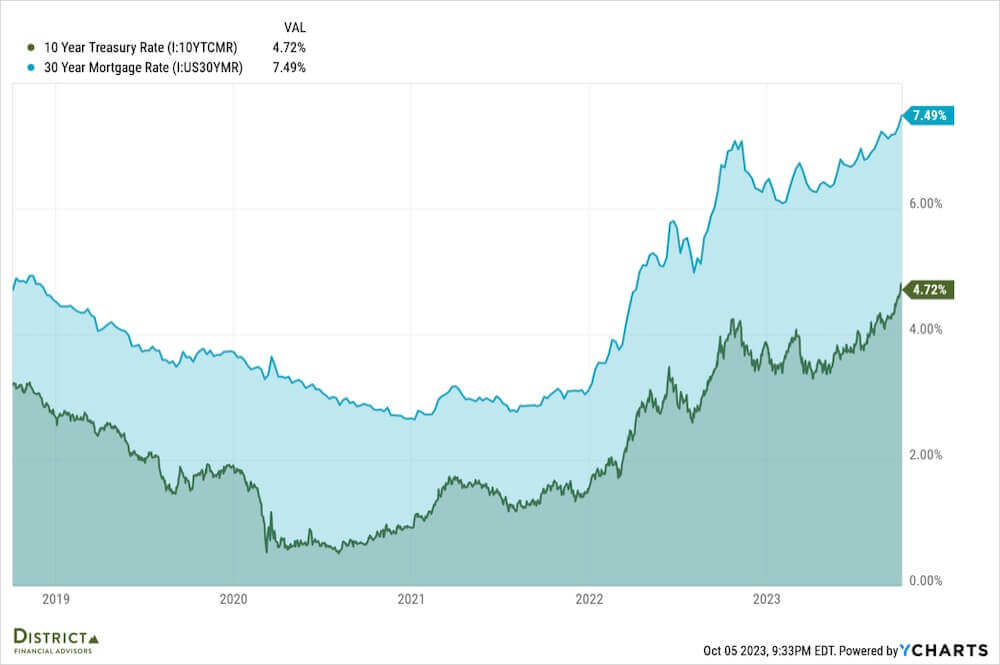

We should instead compare the idea against an investment that would be considered very conservative or even risk-free, something like a 10-year Treasury bond, a CD at the bank, or a high-yield savings account where there’s very low or no risk.

Now, if you locked in that low rate, things are probably working in your favor right now.

Let’s take a look at this chart of 30-year mortgage rates vs. the 10-year Treasury. You can see the 10-year Treasury rate is currently around 4.7%. If you’re locked in with a mortgage rate in the 3%-4% range, you’re finally on the right side of things after a long period of very low yields on conservative assets.

Now, of course, I’m not against investing extra cash flow in something riskier to go after higher returns. After all, that’s the name of the game, right?

Maybe you want to continue with that type of strategy. Just remember, future returns may not be what they’ve been in the past. This could be a nice way to balance what you’re doing from a cash flow standpoint – building assets in different locations on the balance sheet.

For folks with newer mortgages and higher interest rates, this is an especially compelling idea right now.

Some Benefits

What are the benefits of timing your mortgage pay-off with retirement?

Lower expenses are at the top of the list for good reason. Eliminating the largest portion of your housing expense can give you a lot more flexibility in the budget. It’s also likely to allow for less stress, not to mention paying off a mortgage usually provides a huge feeling of accomplishment. You really can’t discount these sorts of things.

There is also the guaranteed return on saved interest. This one is straightforward.

If relocation is part of your plan for retirement, being mortgage-free may make it easier. With a cash asset, you could be a cash buyer when the time comes – all you need to do is sell your home. If you’re buying a property in a similar or lower price range this can also really work in your favor.

Lastly, two very important things.

It may allow you to take the pressure off claiming Social Security when you turn 62. We know when you claim benefits at 62, it’s a 30% reduction from what you can receive at full retirement age.

No mortgage payment may also allow you to delay taking income from your investment portfolio. When taking income from your investments, the sequence of returns becomes very important. If you don’t need to take anything or can take less from your account, that works in your favor and reduces the stress on your portfolio.

In contrast, it’s only fair to mention drawbacks. Liquidity is a big one; houses are not liquid assets. There’s also opportunity cost – could you use that money somewhere else? And of course, are you giving up higher returns?

Where does timing a mortgage payoff work well?

I think this plays well for people who are 10 years or more from retirement, mostly due to the impact making incremental payments over time can have.

It’s also essential to have the extra cash flow available to put towards your payoff goal that’s not going to take away from your retirement plan or other parts of your long-term vision.

If you have strong feelings about being debt-free, this is a win.

If you want to reduce your monthly expenses and take stress off the budget, this is another nice benefit.

And, if you don’t have competing goals like buying a vacation home, investing in real estate properties, or similar ideas, this is a logical place to direct additional resources.

Where doesn’t this work and what should you avoid?

If you have five years or less until retirement, I think it makes sense to use your cash flow in other places to give yourself flexibility. Stack your resources and make decisions when you hit retirement.

If you’re not planning on staying in the home for the longer term, I don’t think this makes sense. If you’re planning to move within the next five years, you may need to figure out the loan situation all over again.

If you love your low interest rate and the idea of getting a higher interest rate at the bank or investing riskier assets like stocks for higher return potential, it may not make sense to pay off your mortgage early.

One big thing you want to avoid is taking a significant lump sum from a pre-tax TSP or IRA account to pay down your mortgage. These distributions are taxed as ordinary income, thereby adding to your tax bill and potentially pushing you into a higher marginal tax bracket.

How to make it happen

Since we determined that lump sums are generally out with this idea, what we’re talking about is making additional incremental payments over time.

Applying things like tax refunds and bonuses when you receive them can be a nice way to pay down an extra chunk of principal.

Making extra monthly payments based on your desired payoff date is at the core of making this work – you just need to find the monthly payment that will allow you to pay off the loan by your planned retirement date. For example, 10 years and $400 extra each month.

If that’s not reasonable, think about something smaller. Our example earlier illustrated the impact that even one extra payment per year can make.

I hope this has given you something to think about within your financial plan. Does this strategy fit? Maybe, maybe not. Let’s make the best decision for your situation. Don’t be afraid to ask questions. I’m here to help.

The content is developed from sources believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material.