We have all heard the arguments for life insurance, including replacing lost income, paying off a house or children’s education, and making sure your family can maintain a standard of living without you.

The decision to provide that important protection for your family is only the first of many critical decisions, though. How much insurance do you need? What types of life insurance are available, and which are right for you? Where can you get the appropriate insurance, and how much will it cost? How does the Federal Employee Group Life Insurance (FEGLI) fit into the equation?

There are many factors to consider and you should consult a professional about your individual situation.

How much life insurance do you need?

There are two primary ways of determining the amount of life insurance you need. The first is using the “income replacement” method, which is based on your current income. Typical recommendations go as high as 10-12 times your salary for someone with a young family, dropping lower as you age and your family situation changes.

The second method of determining life insurance requirements is the “actual needs” method. In that case, you would add up the expenses that the insurance should pay for if something happened to you. Some examples of what that could include are:

- Final expenses

- Mortgage payoff

- Credit card and other debt

- Children’s education

- Needed income supplement for spouse

- Child’s wedding

- Funding a spouse retirement account

- Emergency fund

The maximum amount of insurance available through FEGLI is roughly six times your salary, utilizing the Basic insurance plus five times Option B. Keep in mind that just because it is the most they offer, doesn’t mean that it is all you need. You should perform your own analysis to come up with an amount you and your spouse are comfortable with.

What types of life insurance are there?

There are several different classifications of life insurance. Variations among them include premium amount and type, cash value and investment options, changes in premiums, and how long the insurance lasts. Here are some brief descriptions of the available types:

Whole Life Insurance

Whole life insurance is the most expensive type of insurance, but is designed to last your entire lifetime. As long as the premiums continue to be paid, your beneficiary will receive the face value at your death, regardless of your age. Cash value builds up in the insurance contract over time, which can be utilized by you during life or added to the death benefit. The cash value earns an interest rate set in the contract and does not vary.

Universal Life Insurance

Universal life insurance is similar to whole life insurance, except that the premiums can vary depending on your ability and desire to pay. Cash value is also built up in the early years, if premiums paid are sufficiently high, and can be used later to help pay for the increasing cost of insurance within the contract. This is the most flexible insurance option with regard to payments, but can be expensive to maintain in later years. If you continue to pay the necessary premiums, though, it will continue to remain in force regardless of your age.

Term Life Insurance

Term life insurance is the least expensive option available and also the simplest. The term of the policy is for a given number of years (typically 10, 20, or 30), and as long as you pay the premium your beneficiary will get the face value at your death. There is typically no cash value in the policy, and once the term is up you no longer owe any premium or are covered by the insurance. This is a common selection to add a large amount of insurance that is needed now, but may not be needed in the future after the term expires.

There are also several companies that offer term life insurance products that may be able to be continued after the term or converted to a permanent insurance policy. They may be more expensive at that point, but options are available.

Variable Life Insurance

Variable life insurance is a variation on a universal life insurance policy that allows for the accumulated cash value in the contract to be invested according to the policy owner’s wishes. The investments are selected from available insurance company managed subaccounts and essentially function in a manner similar to mutual funds.

What is Federal Employee Group Life Insurance (FEGLI)?

The FEGLI program is a type of contract called a “group term” policy. You are covered for a set amount (a multiple of salary) for as long as you are employed and pay the premium. Once you are eligible for the program, there is no medical exam or other limitations on participation. This can make it an attractive option for those people with existing health conditions, poor driving records, or dangerous jobs.

Federal employees are automatically enrolled (though you can opt-out) in the “Basic” plan, which covers your salary (rounded up to the nearest thousand, plus $2,000) and is partially supplemented by the federal government. For postal employees, Basic insurance is paid completely by the USPS. The Basic plan also offers double the Basic insurance death benefit to those under age 35 free of charge, which then gradually reduces until age 45 is reached and the extra benefit is eliminated. “Option A” is an option to add $10,000 of insurance. “Option B” allows you to add a multiple of your salary to the insurance amount, up to five times. Option B pricing is based on your current age and adjusts at every five-year interval (where your age ends in a 5 or 0). “Option C” provides some insurance protection for your spouse and dependents, in multiples of $5,000 and $2,500, respectively, up to five times that amount. None of the options other than Basic is supplemented.

Increases to the FEGLI selected options can only be made at certain times. Those include initial enrollment, as a result of a change in the family (marriage, children born, etc.), and open enrollment periods. Open enrollment periods are rare, however, and should not be relied upon to make changes. The last two were in 1999 and 2004. Decreasing the level of insurance can be done at any time.

In the case of federal employees, there are also various options available after retirement. When considering retirement, a federal employee should consult with someone familiar with the FEGLI program before making their selection.

What do alternatives to FEGLI cost?

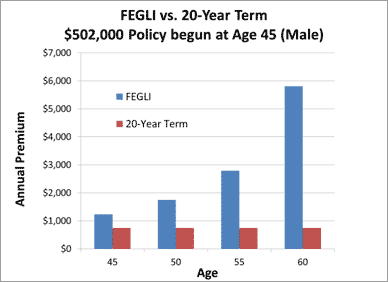

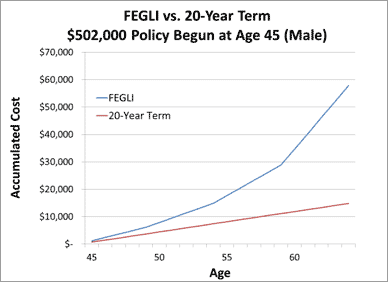

The actual cost of life insurance will depend on the type and the amount. A popular alternative to FEGLI is a 20-year term policy, which can provide cost effective coverage for the length of time that it is most needed. As an example, a male federal employee making $100,000 per year with a 4x Option B selection would have a total of $502,000 of insurance through FEGLI. At age 45, the FEGLI premium is $1,230 per year. For an equivalent 20-year term policy, premiums could be as little as $743 per year for a non-smoker in good health. The numbers are even better for a female, due to the increased life expectancy, with an annual premium possibly as low as $598. While that is just a single example, the benefits are similar at any age.

It is also important to keep in mind that the costs of the 20-year term are held fixed for the 20 years, while the cost of FEGLI Option B will continue to increase as a new age bracket is entered. For example, the 45 year old male would save over 74% over 20 years with the term policy.

The following charts demonstrate the effect:

In addition to a term policy like the given example, another common alternative to FEGLI are other group term plans. Some of these insurance companies or associations may have lower premiums than FEGLI in some instances, but still base premiums on 5 year age intervals. This can lead to a similar result when comparing costs over time.

Why keeping FEGLI may be a good idea?

While there are potential cost savings by getting life insurance outside of FEGLI, there are also several good reasons why staying in the FEGLI program could make sense in your particular situation. The first is that outside insurance may be too expensive or not available due to a health, lifestyle, or occupation limitation. In that case, FEGLI may be your only option for adequate coverage.

Another benefit to FEGLI is the option to take reduced amounts in retirement. For someone who carries the Basic plan until retirement, they are eligible for the 75% reduction option. In effect, you end up with a policy that has a face value of 25% of your ending Basic benefit (after gradual reductions beginning at age 65) that lasts for the rest of your life, but you don’t pay any premium after age 65. This can be useful in providing a benefit to cover final expenses at no cost to a retiree. That type of benefit would not be available elsewhere.

What should you do now?

The first thing you should do when considering life insurance is to figure out the amount you need. I gave some examples of calculation methods earlier, but a financial advisor can also help you determine an appropriate amount for your particular situation.

After determining the right amount of insurance, the next step is to evaluate your available options. For many people, FEGLI is the best (or only) option available. If you are healthy and have a need for a higher level, though, it often makes sense to look elsewhere for an appropriate plan. If that is the case, be sure to leave your current FEGLI coverage in place until a new policy is issued and in force. Also, be sure to evaluate the different types of insurance available, including various combinations that may be appropriate for you. A professional who is familiar with the FEGLI program will be able to guide you through the options and help with your decision.

Finally, if you are able to find a way to reduce the cost of your life insurance, I recommend re-directing the money you save to your TSP account. This is a great opportunity to increase your savings for retirement without feeling a pinch in your regular budget.