As a federal employee approaches retirement, a very natural thing to do is to request a pension estimate from their HR.

This document can be a great start in knowing what sort of income you’ll have in retirement. But unfortunately, agency estimates are not perfect, or in some cases, simply incorrect.

It is so important to know what you are truly eligible for so that you don’t have any unpleasant surprises at retirement.

Too many employees have received letters from OPM letting them know that they actually aren’t eligible for retirement or won’t be getting as much as they thought.

Common Mistakes

An agency estimate is only as good as the data that is used to generate it and sometimes your agency may not have all the facts.

Your agency (as well as OPM when you retire) will primarily be looking at your OPF (official personnel folder) to find information about your career to calculate your pension. If you don’t know how to access your OPF then the first step is to contact your HR for instructions on how to do that.

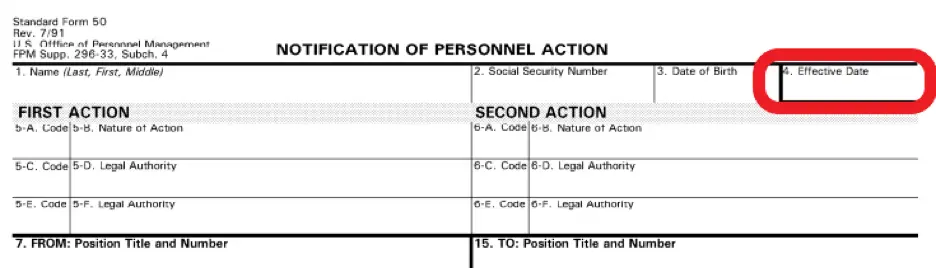

One key document that you’ll find in your OPF is your SF-50’s. You will most likely have a few dozen of these depending on how far you are through your career. You will want to make sure that all position/agency changes are accounted for in your SF-50’s. It is not uncommon for some agencies to not forward your records on to your next agency.

One of the first things to check is your effective date of your first SF-50 when you were first hired. This will help ensure that your creditable service is calculated correctly. This is usually found near the top of the page.

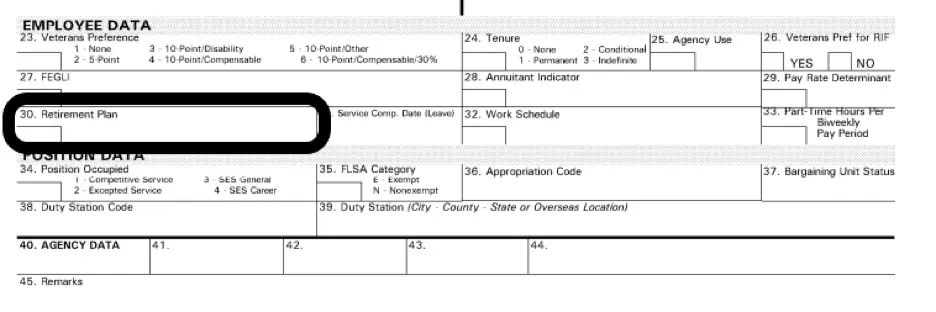

One of the next things to check is that you are in the right retirement plan throughout your entire career. For the vast majority of traditional FERS should have something that says “FERS and FICA” in box 30. This means that you are paying into the FERS retirement system as well as Social Security.

Things to Watch For

Mistakes are common when you are one or more of the following in your career.

- Temporary Service

- Intermittent Service

- Bought Back Military Service

- Leave Without Pay for More Than 6 Months in a Calendar Year

If you have had any of these types of service then you will want to make sure everything is well documented in your OPF and you will want to know exactly how that time will affect your retirement.

I have seen many people have to pay for their military time twice because it wasn’t well documented the first time. Making sure you have the correct documentation in your personal possession can help avoid this type of situation.

Keeping Your Coverage

To keep your FEHB and FEGLI in retirement you are required to be covered by these programs for the 5 years before retirement. You will want to make sure this coverage is well documented as well.

If you and your spouse are federal employees then it is likely that one of you is covered under the other’s FEHB plan. Just make sure you have this well documented so that both of you can keep FEHB in retirement.

Final Thoughts

Once you are sure your service is well documented, the next thing to double check is your NET pension. Or in other words, after everything comes out of your pension (i.e. taxes, FEHB premiums, survivor benefits, FEGLI premiums etc) what is left.

A really common mistake I see on agency estimates is that the assumed amount for taxes is often far too low. This often happens because the estimate software assumes that your pension will be your only source of income. But for most federal employees, this is simply not the case because of your TSP and Social Security.

And while checking all these details may seem like overkill, it is often so much easier to fix any issues during your career instead of finding out once you’ve already retired. A little work now can make a massive difference later.