I do not like making mistakes. I am kind of a perfectionist in that way.

I like things to be done perfectly the first time.

But as we all know, it is just a matter of time before we all make a blooper and sometimes these bloopers get pretty big.

Fortunately, there is a ‘do-over’ button for most things in life where we can have another crack at it.

But unfortunately, when it comes to retirement, there are some mistakes that don’t really have a ‘do-over’ button and which can prove to be quite costly.

Here are 3 retirement mistakes that you are certainly going to want to avoid the first time.

Mistake #1: Net Vs. Gross

During our careers we get used to talking about gross numbers. When someone asks us about our salary, we think of our gross salary which is the biggest number on your Leave and Earnings Statement.

But as we all know, the amount that actually hits our bank account every 2 weeks is generally a very different number.There are a lot of things that come out first like taxes, insurance premiums, and TSP contributions.

And the net number (after everything comes out) is what you actually get to live off of.

When you are planning your retirement, you will want to make sure that your net retirement income (after everything that comes out) is going to provide you with the retirement that you desire.

For example, here is a chart of deductions that come out of your retirement income to get you from your gross to net.

| Type of Retirement Income | Pension | TSP | Social Security |

| Potential Deductions | 1. Survivor Benefits (if elected) 2. Health, Life, Dental, Vision, and Long Term Care Insurance Premiums (if elected) 3. Taxes | 1. Taxes (when drawing from the traditional TSP) | 1. Taxes 2. Medicare Part B Premiums (when applicable) |

Note: Whenever requesting a pension estimate from your HR, make sure the estimate is assuming a realistic deduction for taxes. I have seen that most agency estimates significantly underestimate taxes.

Calculating your net retirement income is the first step in deciding if that amount will provide you with the comfortable retirement that you want.

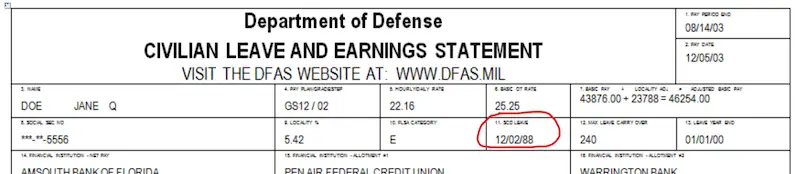

Mistake #2: SCD Vs. RSCD

SCD stands for Service Computation Date and can often be found on your LES (leave and earnings statement like this example:

However, the problem with this date is that it is used for leave purposes only.

The date you’ll want to calculate your creditable years of service for retirement is your RSCD or Retirement Service Computation Date.

While your SCD and RSCD can sometimes be the same, they will often be different, especially if you have had any of the following:

- Military time

- Temporary time

- Bought-back time

- Other irregular service

The first place to go to find your RSCD is to talk to your agency so they have a chance to review your career.

Making sure you have the right date is crucial in knowing exactly when you are eligible to retire. The last thing you’d want is to be told that you have to work another 6 months right when you thought you were about to retire.

Mistake #3: Retirement Paperwork Mistakes

Many of us have seen the YouTube videos of the runners that were in front the entire race but got cocky and tripped right before the finish line, and when people select the wrong things on their retirement application it reminds me of this cocky runner who tripped right at the end.

Don’t let this be you.

Your retirement application is the place where you make a number of really important decisions such as what to do with survivor benefits, FEGLI (life insurance), and taxes.

Make sure you understand the decisions you are making and be sure to get help if you don’t.

You will thank yourself over and over again for doing it right the first time.