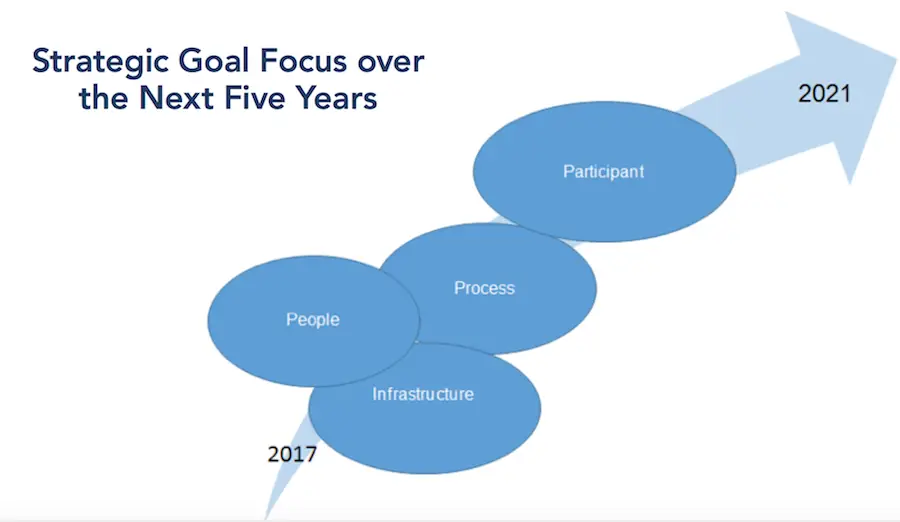

The Federal Retirement Thrift Investment Board has just announced its key goals for the 2017–2021 Strategic Plan:

- Goal A – Implement a physical and technology infrastructure that optimizes and supports plan administration, agency operations, and the evolution of a new participant experience

- Goal B – Ensure that the FRTIB has the right skills, competencies, and leadership at all levels

- Goal C – Optimize business processes to allow continuous improvement of TSP and Agency operations

- Goal D – Develop a new participant experience that enables participants to identify and achieve their targeted retirement outcomes

Additional withdrawal options

Included in this strategic plan under Goal D (2.1.) is the intent to implement additional withdrawal options to accommodate post-retirement needs. Presently, the TSP allows only one partial withdrawal which is very unfriendly.

Consider this situation: Tina has retired after working for the federal government for 35 years. She and her husband Tony have decided to celebrate their new journey by going on a 10-day Mediterranean Cruise. They had a fabulous trip but come back to find that their 30-year roof needed to be replaced.

“No fear,” Tony tells Tina. “The savings in our bank account will cover half of the cost, and perhaps you can withdrawal $10,000 from your TSP.”

Tina agrees, and the next day she contacts the TSP and is shocked to learn that she is not able to withdrawal another lump sum from her account, since she has already used up her one-time partial withdrawal pass.

Roth and traditional balances

As many of you know, I am a proponent of tax efficiency in retirement. Our national debt is over $19 trillion and growing. Our country’s entitlement programs, particularly Medicare and Social Security, are severely underfunded.

Each year, Uncle Sam gets to tell you his share of your traditional TSP distributions. However, he can’t take ownership of your Roth TSP, provided you follow the 5-year and 59 ½ rule.

The problem at present is that everything comes out proportionately and cannot fully utilize the benefits of tax efficient planning. Goal D (2.2.) under the FRTIB Strategic Plan would implement the capability to invest and withdraw Roth and traditional balances separately to facilitate participant tax advantages.

Keep in mind that these are goals, so they do not guarantee these changes will go into effect by 2021. There are many other goals included in the FRTIB’s strategic plan, but these were two of them that hit home since I am a retirement planner for federal employees.

The full 2017 – 2021 Strategic Plan is included below.