There are a lot of resources for explaining how the Federal Employee Health Benefits (FEHB) Program can work with Medicare. The Office of Personal Management has a 20-page guide, The Federal Employees Health Benefits Program and Medicare, which answers “how the FEHB Program and Medicare work together to provide health benefits coverage to active or retired Federal employees covered by both programs. It explains what Medicare does and does not cover, who is eligible for Medicare, and how benefits are coordinated between Medicare and FEHB plans.”

The OPM guide is dated 2008. Hotlinks contained within the online PDF appear to be current. Some information, however, such as The Part B premium for 2008 ranges from $96.40 to $238.40, but will be adjusted annually, and terms such as the one for Medigap scream for updates. Perhaps AI will answer the call?

There is no mention, however, in the guide explaining an important benefit for federal annuitants who opt for Medicare and an FEHB plan. This advantage is ideally no emails or phone calls from collection agencies.

Unpaid Medical Bills Among Older Americans

The Consumer Financial Protection Bureau (CFPB) implements and enforces Federal consumer financial law and ensures that markets for consumer financial products are fair, transparent, and competitive. On May 30, 2023, it released a document in its Issue Spotlight series, Medical Billing and Collections Among Older Americans.

The Medical Billing and Collections Among Older Americans used data from the Census Bureau’s Survey of Income and Program Participation. The CFPB also examined consumer complaints submitted to the agency between January 2020 and December 2022. Among its findings:

- Older adults complain of a complex medical billing experience

- Almost four million adults over the age of 65 had unpaid medical bills in 2020

- Unpaid medical bills for older Americans increased by 20 percent in 2020

- Medical billers and providers refer inaccurate medical bills to collectors and credit reporting companies thus having an emotional and physical toll on older adults

- Almost 70 percent of these older adults have medical insurance coverage from two or more sources

- Older adults are more prone to have issues with their abilities to detect and correct inaccurate medical bills

The medical billing and collection system devotes insufficient resources to preventing, identifying, and correcting errors. Inaccurate medical billing affects consumers of all ages according to the CFPB. Older adults are more prone to be victims of errors and inaccurate bills because of two key factors.

The first factor is older adults more so than younger adults are more likely to have multiple chronic health conditions which require medical care. Older adults with chronic conditions need higher-level care resulting in billing codes with larger payments that require detailed claim documentation.

The second factor is older adults usually have multiple insurances – increasing the complexity of the billing process.

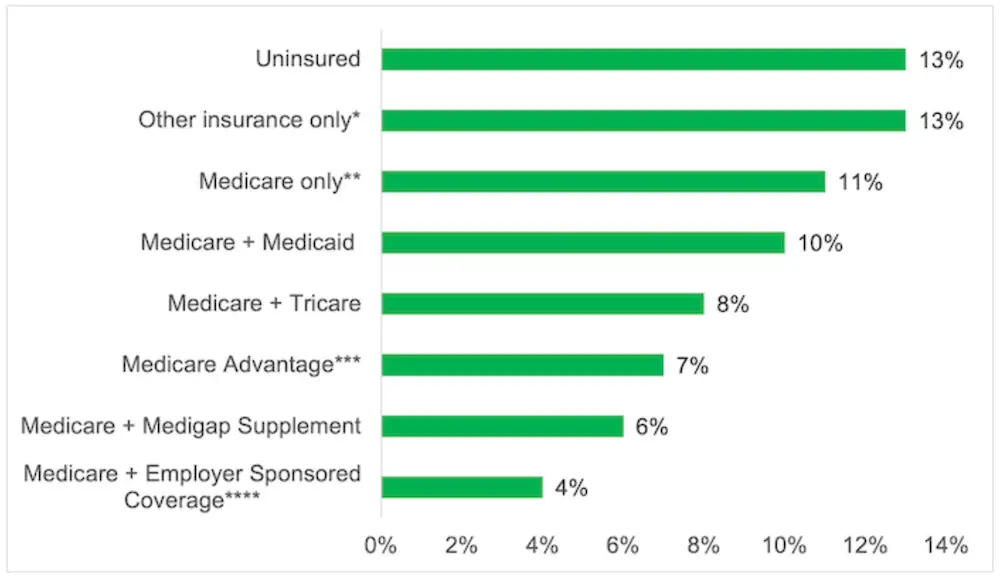

The good news is that unpaid medical bills seem to be less of a problem when Medicare is paired with an employer or former employer’s health care plan. This combination results in the best partnership as displayed in the accompanying chart from the CFPB’s report.

Percentage of older adults reporting unpaid medical bills by selected sources of coverage, December 2020

FEHB and Medicare Options

As you reflect on whether to combine your future FEHB coverage options with Medicare here are some additional aspects to consider.

First, FEHB and Medicare premiums provide you with a sense of budgetary certainty. The premiums for each are monthly expenses. This is an alternative to facing catastrophic financial costs for expensive medical procedures. If one decides on having only Medicare or only FEHB that means one has to increase the liquid assets in one’s investment portfolio for the contingency of expensive future bills for medical emergencies.

Also, the FEHB program provides you with a menu of updated health plans. You will have to do some homework to find the specific plan that works best for you. In retirement, your healthcare needs may change as you age.

Remember there are three main types:

- Preferred Provider Organization (PPO) and Fee-for-Service (FFS) plans,

- High Deductible (HDHP) and Consumer-Driven (CDHP) plans,

- and Health Maintenance Organization (HMO) plans, some of which have Point-of-Service (POS) benefits outside the plan network.

All the plans annually compete for your choice during open season and all plans can be compared through the FEHB Plan Comparison Tool.

Finally, think of the FEHB plans as advocates for you and your spouse. The FEHB plan, not you, receives the bills for whatever Medicare does not cover. You will have visibility of the billing process and be kept informed of the process but there may be no additional bills that require your checkbook or credit cards.

My spouse and I, after several years of Medicare and the FEHB partnership, have never experienced any bill payments or collection agency episodes. Our FEHB plan takes care of all deductibles, coinsurance, and other expenses thus far. We even get a generous rebate from our FEHB plan for our enrollment in Medicare.

The FEHB and Medicare bill coordination may not be a perfect fit for everyone. The right FEHB plan combined with Medicare may mean the absence of a collection agency in your case. Maybe OPM should emphasize that aspect of the FEHB and Medicare partnership the next time it updates The Federal Employees Health Benefits Program and Medicare pdf.