The Thrift Savings Plan (TSP) is designed to provide financial security for federal employees and service members during their retirement years. However, it also ensures that those benefits continue to support loved ones after a participant’s passing.

Upon the death of a TSP participant, the plan initiates a specific process to distribute the remaining account balance to designated beneficiaries. Depending on the type of beneficiary and their relationship to the deceased, different procedures and options become available, ensuring the smooth transfer of assets and continuation of the TSP’s mission to provide financial well-being.

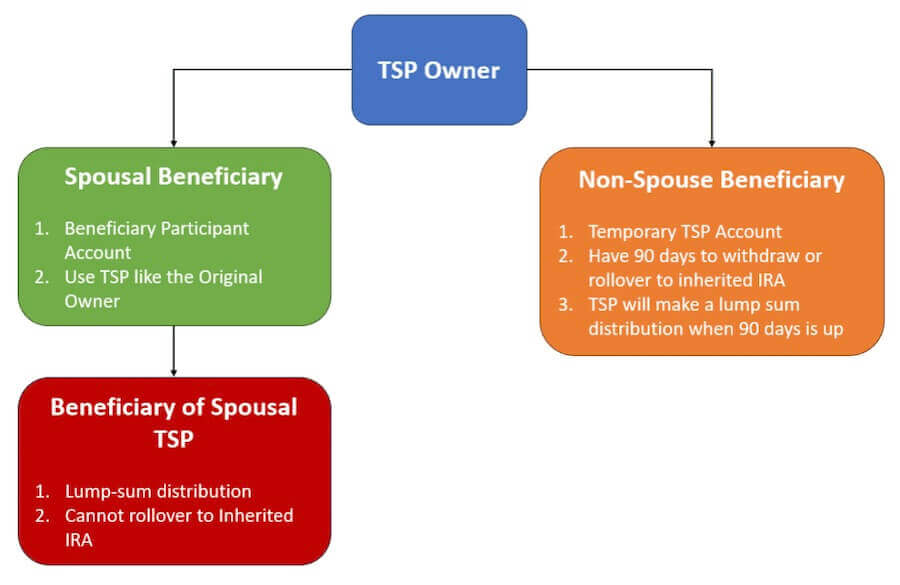

Types of Beneficiaries

There are two primary types of beneficiaries under the TSP:

Spouse Beneficiary

If a participant designates their spouse as the beneficiary, the spouse becomes a TSP beneficiary participant account upon the participant’s death. The beneficiary participant account functions similarly to a regular TSP account, allowing the spouse to continue investing and withdraw.

Non-Spouse Beneficiaries

Non-spouse beneficiaries include children, other family members, or trusts. Upon the participant’s death, a temporary TSP account is established for non-spouse beneficiaries, who can receive the funds through various methods, such as a single lump sum payment, installments, or transferring the funds to an inherited IRA. They only have 90 days to make a decision. After that, the TSP will automatically pay the lump-sum total distribution to the beneficiary.

Payment Process for Spouse Beneficiaries

The payment process for spouse beneficiaries is relatively straightforward:

- Beneficiary Participant Account: Automatically establish a beneficiary participant account in the spouse’s name.

- Investment Options: The beneficiary participant can maintain the existing investment allocations or choose different investment options.

- Withdrawals: The beneficiary participant can withdraw as needed, subject to TSP rules and regulations.

- Required Minimum Distributions: The TSP will assist in calculating the RMD amount based on the ages of the participant and spouse.

Payment Process for Non-Spouse Beneficiaries

The payment process for non-spouse beneficiaries is slightly different:

- Temporary TSP Account: A temporary TSP account is created to hold the deceased participant’s TSP balance.

- Payment Options: The non-spouse beneficiary has 90 days to choose a payment option, including a single lump sum payment, installments over time, or a transfer to an inherited IRA.

- Automatic Payment: If no payment option is selected within 90 days, the TSP will automatically disburse the funds as a single lump sum payment.

Payment for Beneficiaries of a Participant Account

Since the spouse can keep the participant account open, they can have their own designation of beneficiary on file. However, when the spouse participant dies, they are forced to take a lump sum distribution from the TSP. They cannot keep the funds in a participant account or roll them over to an inherited IRA.

TSP Beneficiary Rules Chart

Verify Your TSP Beneficiary By Chat with AVA

The TSP now has AVA, the virtual assistant that can answer questions regarding your account and verify beneficiary information. You will need to log in to your TSP account then click on the blue “birdlike” circular icon to get started.

Even you are not logged in, you can use the virtual assistant and find general information on the website. Make sure you avoid sharing sensitive information without logging in first.

Factors Affecting Payment

Several factors can affect how the TSP pays beneficiaries, including:

- Beneficiary Designation: The participant’s designated beneficiary, as stated on their TSP account, determines who receives the death benefits.

- Payment Option Selection: The chosen payment option determines how and when the beneficiary receives the funds.

- Tax Implications: TSP death benefits may be subject to income taxes, and beneficiaries should consult with a tax advisor to understand the potential tax consequences.

Important Considerations

- Review Beneficiary Designation: Participants should regularly review and update their beneficiary designation to ensure it reflects their current wishes. If no information is on record, the order of precedence will be used.

- TSP Beneficiary Form: The preferred way to update your beneficiary information is on tsp.gov. You could use the TSP-3 form to update, but the information may not show up online.

- Communicate with Beneficiaries: Participants should inform their beneficiaries about the TSP and its death benefits so that they are prepared in the event of the participant’s death.

- Seek Professional Guidance: Beneficiaries may want to seek guidance from financial and tax advisors to understand the best options for managing the TSP death benefits.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security. Securities and advisory services offered through Osaic Wealth, Inc., member FINRA, SIPC. Osaic Wealth is separately owned and other entities and/or marketing names, products or services referenced here are independent of Osaic Wealth. Representatives may not be registered to provide securities and advisory services in all states. Branch address: 10701 Parkridge Blvd, Ste 130, Reston, VA 20191. Branch phone: 571-543-2783.