The Thrift Savings Plan now allows in-plan Roth conversions, and the questions have started rolling in.

- “How much can I convert while staying in the same tax bracket?”

- “I don’t want to leave taxable money to my kids. What should I be doing each year?”

- “Should I just fill up the 22% tax bracket with conversions?”

All of these sound like reasonable questions, and this is where people get into trouble. I see federal employees making decisions based on information that even AI and financial professionals get wrong. The result is that they end up paying more in taxes over their lifetime, not less.

Let’s walk through the landmines to avoid when using this new feature.

Why Roth Planning Matters More Than Most People Think

One of the biggest misconceptions in retirement planning is that success comes down to how well your portfolio performs. That’s only part of the equation, and in retirement, it’s not nearly as important as you might think.

What really matters is how much you keep after taxes. For many federal retirees, taxes become one of the largest expenses in retirement. That’s especially true for those with significant balances in pre-tax accounts like the TSP. That’s where Roth planning comes in.

Done properly, it can help reduce lifetime taxes and create more flexibility. Done poorly, it can do the opposite.

The Problem with Large Pre-Tax Balances

Good discipline over a federal career can mean that you’re sitting on a healthy TSP account. But large pre-tax accounts come with a hidden issue: Required Minimum Distributions.

RMDs are forced income. You don’t get to choose whether to take them, only when they begin and how much you’re required to withdraw.

And once they start, they can create a ripple effect:

- Higher tax brackets

- Increased Medicare premiums

- More of your Social Security becoming taxable

- Fewer options to manage your tax situation

This is how many federal retirees end up with what I often call a “tax bomb.”

The Valley Opportunity

There’s a window of time where planning becomes especially valuable. After you retire, but before RMDs begin, your income often drops. You’re no longer earning a salary, and forced distributions haven’t kicked in yet. Sure, TSP withdrawals count as taxable income, but you likely don’t need to withdraw as much as you earned in salary leading up to retirement.

This period is what I refer to as the Tax Valley. During this window, you have more control over your taxable income than at almost any other time in your life. That’s often when Roth conversions can be most effective.

That said, this isn’t the only time conversions can make sense. With tax rates historically lower than they’ve been in the past, there are situations where converting earlier, even while working, may still be worth considering.

The key is not the timing alone. It’s how the decision fits into the bigger picture.

What Changed Inside the TSP

As many of you know by now, the ability to do in-plan Roth conversions is a meaningful update. You can now move money from Traditional TSP to Roth TSP without transferring it to an IRA.

That’s convenient. But convenience doesn’t mean it’s the right move. A Roth conversion creates taxable income in the year you do it. In the TSP, the taxes need to be paid from outside the account. Unlike other situations, the TSP doesn’t make that as flexible, so you need to be intentional about where those tax dollars come from.

This alone can make or break whether a conversion makes sense.

The Biggest Mistakes

There are a few patterns that come up consistently when I meet with federal retirees:

- Converting too much in one year. This often pushes people into higher tax brackets without realizing the full impact.

- Looking at tax brackets alone. It sounds logical, but it’s incomplete. Your marginal tax bracket is only one piece of the puzzle. It doesn’t account for potential loss of deductions and other tax potholes.

- Ignoring Medicare IRMAA thresholds. A small increase in income can trigger a large increase in premiums, even while staying in the same tax bracket. These are hidden taxes.

- Overlooking capital gains and NIIT. If you have assets outside of retirement accounts, these layers of tax matter.

- Treating Roth conversions as a one-time decision. This is not a “set it and forget it” strategy. It needs to be evaluated year by year and often multiple times in the same year depending on how your year progressed.

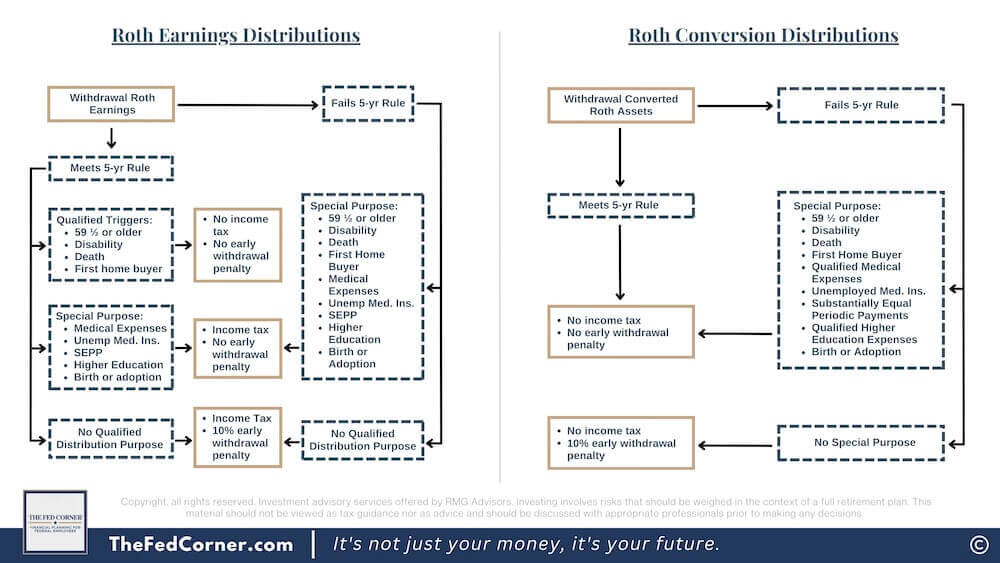

The 5-Year Rules Even AI Gets Wrong

One of the most misunderstood parts of Roth planning is the five-year rule. In reality, there are multiple five-year rules, and they apply differently depending on:

- Whether you’re dealing with contributions or conversions

- How long the account has been open

- When the growth occurred

Getting this wrong can lead to unexpected taxes or penalties. It’s more nuanced than most people realize, and it’s an area where mistakes are common. See below for a visual of how the rules work: