Rising prices can have nasty consequences especially for those on a fixed income, such as federal retirees.

But I have good news for you; as a federal employee, there are some things you can do to protect your retirement.

Know The Game

As a federal employee, some of your retirement income is naturally protected from inflation, but not all of it is. Here are the main sources of income you’ll have:

- Social Security

- FERS Pension

- Thrift Savings Plan (TSP)

Social Security will automatically receive COLAs (cost of living adjustments) which means that in retirement your Social Security benefits will go up as inflation/prices go up.

Your FERS pension does get COLAs as well, but there are two catches:

- The COLAs don’t start until age 62

- If inflation is higher than 2% then the COLA will lag inflation by a little bit.

But overall, your FERS pension (after age 62) will keep up with inflation pretty well.

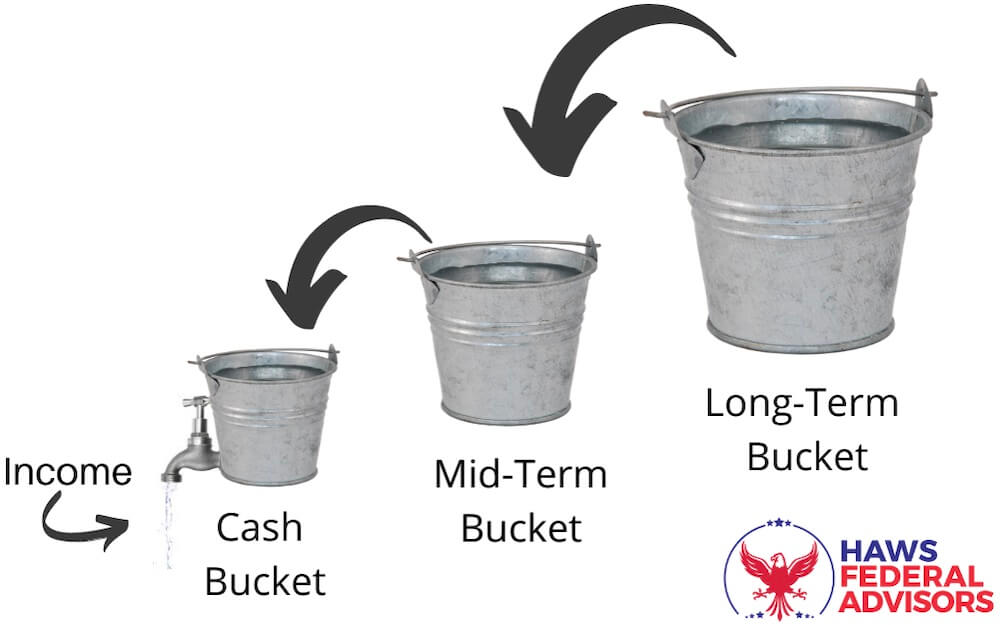

Can My TSP Keep Up With Inflation?

Your TSP certainly has the ability to keep up with inflation, but it is up to you to make sure it does as it won’t happen naturally like Social Security.

The way you are able to do that is by investing it in way that will ensure these two things:

- Your short-term money is safe and not volatile.

- Your long-term money is beating inflation and ensuring that you never run out of money.

This can be accomplished by using the bucket system. Spoiler alert: You shouldn’t be 100% invested in the G Fund. 🙂

No Variable For You

Another great way to protect yourself from inflation in retirement is getting rid of anything that you have to pay a variable rate on such as a variable rate mortgage or even credit cards.

Long story short, as inflation increases, the government generally increases interest rates which means that all variable rates will increase along with it, so if you have a variable rate mortgage, look at other options. Likewise, if you don’t currently pay off your credit cards every single month, then now is the time to come up with a plan to pay them off.

I Don’t Like Cash (Sometimes)

Cash is king, right? Well not all the time.

Having cash in the bank is great when you need that money soon as it is safe and not volatile. However, high inflation means that cash that isn’t growing and is losing value every single day, so any money that you don’t need soon should often be invested in something that will grow (at least a little) over time.

But the good news is that because interest rates have increased, nowadays you can find high-yield savings accounts that are paying as high as 4% (as of writing March 2023). You can find some good high-yield savings accounts here.

The Best Protection of All

The most important thing you can do to protect yourself from inflation in retirement is by having some wiggle room in your retirement numbers. If you barely have enough income in retirement to keep up your desired lifestyle then things are going to be stressful.

Going into retirement with some margin in what you have and what you need is the best way to be confident in your retirement.