I talk a lot about retirement planning, and one element that can’t be neglected is how to properly structure a portfolio. As a federal employee, your Thrift Savings Plan (TSP) is likely the largest asset you own, and you want to make sure you’re doing the best job you can at maximizing it through your retirement years.

Design Portfolios Around Economic Seasons

Like the weather, there are seasons in the economy. I don’t mean to minimize the complexity of economics, but there are only four seasons federal employees need to consider.

Periods of economic growth are typically followed by inflation, which causes rising interest rates and subsequent contraction in the economy, leading to economic decline. Eventually the economic decline is sufficient to curb inflation, at which point interest rates begin to ease and reduce, acting as stimulus for new economic growth once more.

This cycle repeats relatively consistently, but an interesting characteristic of economics is that the amount of time between different seasons is not consistent. It could be as little as months or as much as years between seasons. There are certain asset classes that are suited for each type of economic season to help you pursue your financial goals.

Assets fall in and out of favor depending on the happenings in the economy. For example, bonds were very unpopular (and notably unprofitable) for many years until just recently once interest rates rose. Today, a strong bond strategy has become a critical part of many retirement plans.

Allocate Assets Based on Your Objectives, Not Someone Else’s

How many federal employees made TSP investment choices based on conversations with friends or colleagues? Or perhaps based on what they heard on the news? Following the hype sets you on a wild goose chase. I’ll prove it.

When the yield curve inverted in mid-2022, financial “edutainment” trumpeted this event as all but an ironclad assurance that a recession was imminent. Here we are, two years later—the yield curve still inverted—and investors who were influenced by them missed out on the markets’ accretion of 40% during the same time. And what of those who never made it back in from the pandemic? They missed more than a double: 120% in four years for the S&P.

You want to create an investment allocation that is designed to support and frame your personal objectives. One family may do more traveling in early retirement, while others may want to fund their grandchildren’s education. Some may be philanthropic while others may want a vacation home for their family. Each of these objectives require a different set of strategies to help you pursue them.

Retiring feds may be eligible for a pension and myriad other benefits, which influence cash flows, taxes, and other parts of their financial plan. Ultimately, federal employees should allocate their portfolios factoring in all elements of their plan.

Below is an example of how one might start to think about aligning their wealth with their objectives.

Utilize Well-Researched Investment Selections

Doing research on investments involves more than simply picking a popular name. In the myriad asset classes you’ll need for your portfolio, is it prudent to stay only within one or two managers?

There are many great choices, like Vanguard, Blackrock, Fidelity, Schwab, American Funds, Dimensional… the list goes on. Does being a good manager make them the best in all asset classes? History tells us otherwise. Each manager has its own strengths and weaknesses. Some funds are better than others at certain objectives.

What if the portfolio manager at a large fund retires? This isn’t hypothetical—it has happened before, with that specific fund no longer being as high-performing as it once was after key-personnel left the organization. They shall remain unnamed but know that they were large and well-known.

Managers often have dozens of options, from stock funds (large, mid, small, value, growth, etc.), bond funds, alternative funds, liquid, and many others. Each have their own approach to achieving those investment policy objectives.

How closely do they stick to their own process? Many managers have failed to follow their own Investment Policy Statements (IPS), and investors in those funds could pay the price as a result.

Diversification of managers helps you have less dependency on any one manager doing their job right, and it may even offer the opportunity to reduce your overall portfolio risk.

For most active federal employees, the TSP’s five core funds are just fine. Your investment needs are likely limited while working, with your TSP’s job singular: grow. In fact, if you still have many years left in your federal career, dare I say: don’t overthink your allocation (although do check with your planners, please).

But retirees have vastly different needs that often require more tools. While many are offered in the TSP’s Mutual Fund Window (MFW), I don’t particularly care for it in its current state for myriad reasons, not to be explored in this column.

How should one filter through the universe of choices? Here’s a guide to get you started:

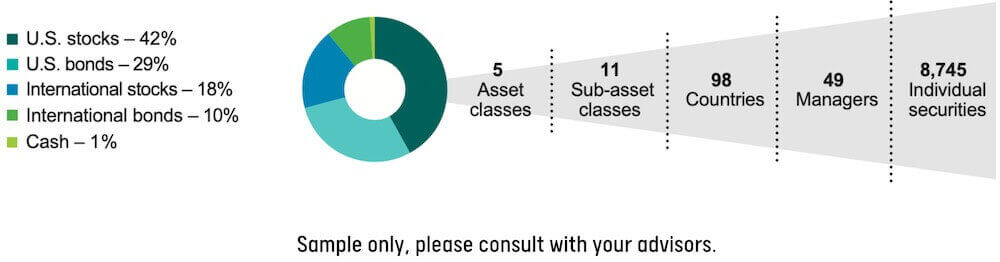

Reduce Risk Through Multiple Layers of Diversification

Your portfolio should have multiple layers of diversification that’s designed to help you optimize return while reducing risk.

People often compare performance of certain parts of the markets without looking at its risk-adjusted rate of return. For example, consider a portfolio of 70% stocks and 30% bonds. There is almost a limitless number of different 70/30 portfolios that can be created all with varying degrees of risk, volatility, and growth potential.

The TSP S Fund often performs better than the C Fund. But better performance today often means more volatility tomorrow. What is their risk-adjusted rates of returns? Which is better for you in the long run?

Not all stocks are created equally, and not all index funds are the same either. There is a greater universe beyond simply the S&P 500 (TSP C Fund) as your choice in equities (stocks).

When developing your own allocation strategy, there are five levels of diversification to consider, making sure each is in accordance with your retirement plan. Think of the vacations you’ll take, the goals you’ll fund, the risks you need mitigated, and then work from there.

- Level 1: Asset classes in general (stocks, bonds, cash, alts, etc.)

- Level 2: Sub-asset classes (large cap, small cap, growth, value, etc.)

- Level 3: Geographic diversification of the portfolio

- Level 4: Individual managers (Fidelity, Vanguard, Schwab, Blackrock, etc.)

- Level 5: Individual securities selected by those managers

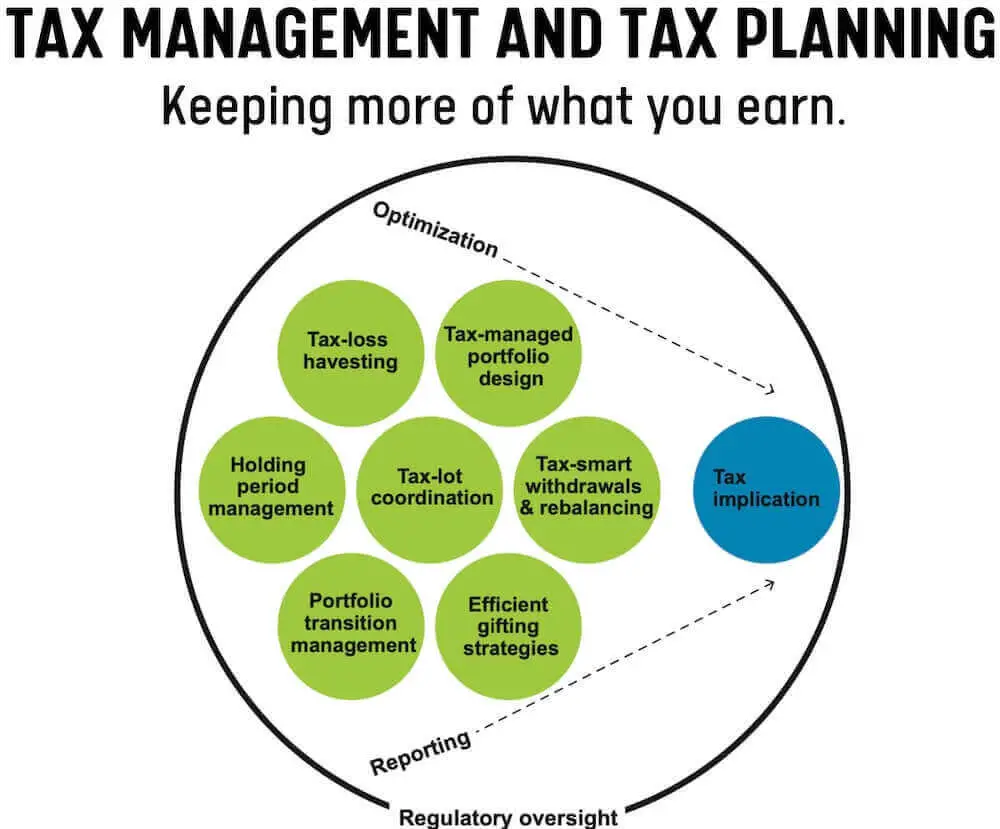

Incorporate Tax Management and Tax Planning

For the better part of a decade, I’ve proclaimed that tax planning is one of the most valuable services an advisory firm can do for their clients. We’re finally seeing the industry start to raise their training wheels.

If you get amazing returns throughout your life but lose a third of your wealth (sometimes more) to taxes, what was your real rate of return? What is your long-term, after-tax rate of return?

You should do everything you can to keep more of what you earn. There are various elements to consider when managing your wealth in retirement, as it’s the first time you have total control over how you generate your “retirement paychecks”. A few of these factors are illustrated below:

I’ve never been a believer in beating the markets, but I do believe in having a diligent approach toward getting the most out of retirement. Your golden years can be the most beautiful and meaningful part of life. You owe it to yourselves to get it right, because it’s not just your money, it’s your future.