Latest on Inflation: Inflation Falls, Consumer Price Increases Slow Down

From reading the news headlines, economic news is all good. The inflation report for the month of July that was just released, reads, “The Consumer Price Index for All Urban Consumers (CPI-U) declined 0.1 percent…after being unchanged in May….Over the last 12 months, the all items index increased 3.0 percent ….”

Another headline after the latest inflation report was released: “Inflation falls in June for first time since 2020 as consumer price increases continue to slow.” That is good news.

How do we stand after the highest inflation in the last 40 years? The reality is that our standard of living has declined despite the rosy headlines that often appear in the news.

Lower inflation is good news. It is also an election year, and Americans generally do not trust the media to report news accurately. In a 2023 poll, 32% of the population had “a great deal” or at least “a fair amount” of trust on what they read in the news.

Here is a summary of the impact of the rapid inflation of the last several years.

Lower COLA in 2025

Older Americans often feel the strain of inflation more than others, and next year’s COLA benefit bump may not offer much relief.

According to the latest estimate from the Senior Citizens League released after the June CPI data was announced, “Our model points to a substantially lower COLA for next year after the 3.2% COLA in 2023. The 2025 COLA prediction is about 2.63%, up from 2.57% last month.”

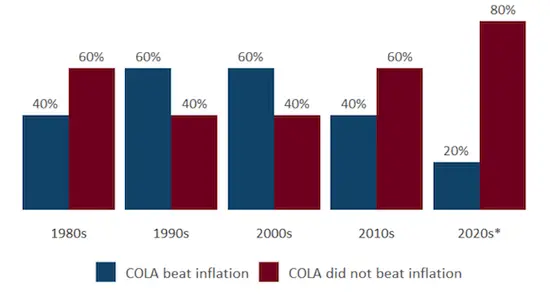

COLAs have become less likely to keep up with inflation. As shown in the chart below, just one of the five COLAs implemented in the 2020s (20%) has outpaced inflation, compared to 40% in the 2010s and 60% in the 2000s and 1990s. This chart is from a Senior Citizens League press release.

COLA vs. Inflation: Inflation Wins

Americans are generally noticing that inflation is impacting their standard of living. It probably has a greater impact on retirees who rely on Social Security.

Federal employees have the added advantage of a regular annuity, Social Security (for those under FERS), and the Thrift Savings Plan. Federal employees are relatively well off with this triad of retirement income sources.

Older Americans feel the strain of inflation, and next year’s Social Security benefit bump may not offer much relief. Food prices were up by 25% from 2019-2023. Housing prices are up 54% since 2019. Most of us feel these changes in our purchasing power. Despite the rosy projections of “transitory inflation” or “slower monthly increase in inflation” or “inflation is down”, our purchasing power has decreased substantially.

Here is a perspective on inflation most people will never read about.

We are surrounded by goods and services born of the great prosperity from 1950 to 2020.

But what we are going through right now has no precedent in any living memory. The inflation is easily the worst in 40 years but maybe the worst since the Civil War. Crucially, it is combined with a dramatic slowing or falling in output, along with a labor crisis. An accurate description would be inflationary depression, arguably worse than the 1930s.

[T]he mitigating factor in the 1930s was that the dollar was growing in value. Therefore savings would yield more purchasing power over time. Right now, we experience the opposite. Money in the mattress is losing value, while money in the bank makes a positive return but only barely.

None of this is being reported properly. The official data is easily debunked and yet reporters on the business page simply do not bother.

Saving Your Aluminum Pie Pans Yet? | The Epoch Times, July 8, 2024

In 1933, a popular song was “We’re in the Money”. It was a glorified view of the economy celebrating the end of the Great Depression as Hollywood joined the Roosevelt Administration in an upbeat view of economic life in America. Here are the lyrics of this pleasant view of life then:

Oh, We’re in the money

The We’re in the Money (The Gold Diggers Song)

Come, on my honey

Let’s lend it, spend it, send it rolling around

Oh boy, we’re in the money

I’ll say we’re in the money

We’ve got a lot of what it takes to get along

And so we’re in the money

Look up, the skies are sunny

As a historical note, to compare reality to the “We’re in the money” view from Hollywood, 24.9% of the country’s workforce was unemployed, and wages were still falling. The depression lasted until 1939.

The inclination of our news media to project a glorious economy has not changed. While the reliability of the news may be different than in the 1930s, the underlying politics may not be that different.

Latest CPI-W Reading and Your COLA

The COLA for the next year is calculated by comparing the change in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from year to year, based on the average of the third-quarter months of July, August, and September.

The Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) increased 2.9% over the last 12 months to an index of 308.054. This is an increase of 2.26% over the third quarter of 2023.

It is too early to know the final COLA for 2025. It will certainly be lower than the last several years. As noted above, it also means the purchasing power of federal retirees, despite the COLA increases, will continue to decline.

Lower inflation is good news. Perhaps the economy will recover and the standard of living will start to improve again. Most of us can research our expenses over the last several years and find examples of inflation on some products and services going up at least 30% and perhaps as much as 100%. As this inflation experience has impacted almost all of us, the impact on consumer spending, income, company financial figures, and personal financial security will become more obvious over time.

The economic stress is not just on a few people because of their poor personal financial decisions. The inflation has not been transitory or limited to a few individuals. It has impacted hundreds of millions. The long-term impact on the economy remains to be seen.