Experience can be a helpful teacher, especially when you can learn and benefit from someone else’s.

This post shares several things new federal employees may wish to consider. Maybe you transitioned from private industry or are a young person just getting your professional career started as a federal employee; either way you may find something useful here.

1. Take Advantage of Your TSP

Rule #1: Always make sure to contribute enough to get the full matching contribution to your TSP. The good news is that new employees are automatically enrolled in the TSP with a 5% contribution—enough to get the full agency contribution. With automatic enrollment, new employees must now opt out of contributing to their TSP accounts, and the default investment option is a lifecycle fund (more on this later).

Agency contributions work like this—there is a 1% automatic contribution that happens no matter what you do, and up to a 4% matching contribution when you contribute 5% of your salary.

Consider increasing your contributions if you can. The maximum contribution amount in 2025 is $23,500 plus a $7,500 catch-up if you are age 50 or over. There is also an even larger catch-up amount of $11,250 if you are age 60, 61, 62 or 63 which is new for 2025.

2. Don’t overlook the Roth TSP

It’s wise to consider if the Roth TSP fits your plan. If you are a younger employee, it’s common to be in a lower tax bracket at the beginning of your professional career than you may be later. In this case, Roth works in your favor; you could pay tax on your contributions now at a lower tax rate and withdraw your money tax-free in the future when you may be in a higher tax bracket.

However, the concept behind Roth contributions is manifold—if you can win the tax rate arbitrage between now and the future that’s great, but there is also an opportunity to create flexibility and choice with future retirement income sources. Leveraging different account types and creating tax diversification offers that flexibility.

Of course, it’s important to revisit your tax situation before deciding on the right contribution mix for you.

Of note: many legacy employees wish they had this option earlier in their careers – the Roth TSP didn’t become an option until 2012.

3. Incorporate tax diversification

Tax diversification is nothing new, but it’s still overlooked.

It works like this: different account types (Pre-tax, Roth, Taxable) carry different tax benefits and rules. By contributing to a combination of account types, you create an opportunity to be strategic with retirement income distributions and their taxability.

While tax diversification can help create flexibility for retirement income, including a taxable account also allows you to plan and access funds for goals that aren’t retirement related. Home purchases, other major spending goals, helping kids, etc.

Maxing out isn’t always the best option. Sometimes spreading your available capital between various account types is a better choice. Utilize traditional and Roth TSP accounts, and don’t overlook the potential of traditional and Roth IRAs as well as funding taxable investment accounts.

4. Leverage Federal Employee Group Life Insurance (FEGLI)

Consider FEGLI until you figure out how much life insurance your family needs and evaluate other options. FEGLI is a great way to protect your family with up to 6x your salary (using basic + option B) right away, and no underwriting is required if you enroll within 60 days of hiring.

Employees are automatically enrolled in the basic option at hiring. If you don’t want it, you must opt out.

FEGLI is a good option with which to get started. It’s also a great option if you may be uninsurable elsewhere. The disadvantage is in the way it’s priced.

5. Understand the FERS Basic Annuity

Pensions are rare and offer an incredibly powerful benefit in your retirement income picture. Career federal employees will get the most out of this benefit based on the way it works.

FERS Annuity Formula = High-3 Average Salary x Years of Service x Multiplier

The calculation for most federal employees will include a multiplier of 1% or 1.1%. For example, if you work 20 years and your multiplier is 1%, your pension amount will be 20% of your high 3-year average salary.

Employees are required to contribute. For those hired after 2014, this amount is 4.4% of salary. The government kicks in the rest to get your benefits where they need to be based on the formula.

You can be eligible for a deferred annuity after 5 years of service.

Curious how much the present value of a basic annuity is worth? Run the numbers–we can help.

6. Beneficiary Designations

Retirement account and life insurance beneficiary designations typically override anything written in a will. Getting these right and updated is important.

Make sure your FEGLI coverage and TSP account – as well as any other retirement accounts or insurance policies – have the correct beneficiary designations.

Also important to understand: if you name a minor child as beneficiary, a minor cannot own legal property and a guardian or conservator may be appointed in this circumstance.

This is also a good opportunity to check in on your overall estate plan.

7. Look at FSA Accounts

Consider using dependent care, health care, and limited expense health care FSA accounts if you have these types of expenses. It’s worth a tax break if you do. However, keep in mind some of this money is use or lose.

8. Get Your TSP Investments Right

This one is a big deal. In fact, it would be at the top if I was ranking this list. If you aren’t invested properly, it can have a significant impact on the ability to reach your long-term goals.

Evaluate which combination of the 5 core TSP Funds work best for you. Consider factors such as goals, time horizon, risk tolerance, and need for income.

Lifecycle fund allocations may not reflect what you really want or need. Outside of that, it’s good to know exactly how and where your money is being invested.

It’s also important not to try to time the market. Get invested and stay invested over the long-term. Change your allocations based on your financial plan, not on headlines or emotion.

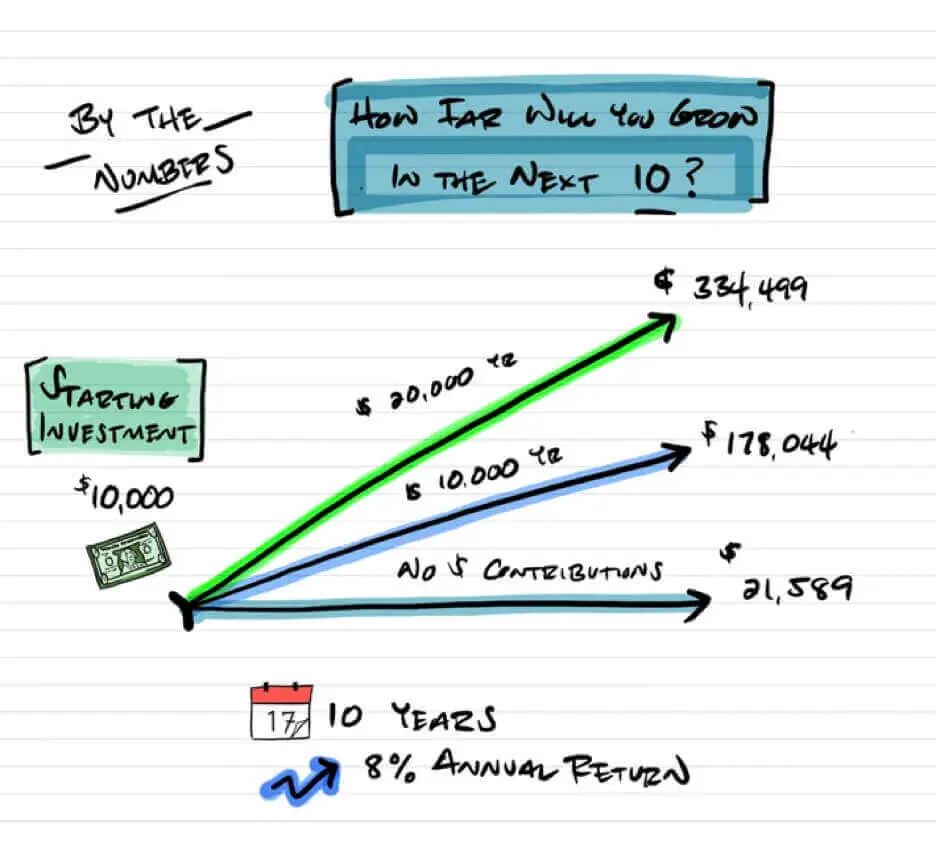

9. Prioritize Saving and Investing

Target investing 20% of your income if possible. It’s fine if you can’t invest that much right now; just start where you can and increase the amount as soon as you can. Extra contributions add up significantly over time.

10. Make a real financial plan

Federal benefits are a wonderful foundation, but they are not a holistic financial plan. A good plan considers the following areas:

- Employee benefits

- Cash flow planning

- Investment Strategies

- Insurance & Risk Management

- Tax Planning

- Estate Planning

Equally important as making the plan is keeping up with changes and updates. It’s not a one-time event.

11. Ask for help and create a support system

Find a mentor or someone you look up to at your agency and engage with him or her. This can be invaluable to helping shape your career path, and be sure to develop and maintain that relationship.

Also consider partnerships with qualified professionals that can help you and enhance your results, such as financial advisors, accountants, attorneys, etc.

What do you think? Do you have anything to add to the list?

The content is developed from sources believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material.