The Thrift Savings Plan (TSP) is pretty amazing in many ways. It’s low cost, easy to use, and offers matching contributions—all of which make it a standout retirement savings option for federal employees. These features make it simple for participants to build a solid nest egg and retire comfortably.

But (and there’s always a “but,” right?), while the TSP shines when it comes to growing your money, it really drops the ball for retirees who are taking money out. It’s a bit like having the best tools to build a house, but no plan for how to maintain it once it’s done.

So here’s the deal: for accumulating money, I give the TSP an A+. For distributing it in retirement? It’s more like a C-. And the main culprit is something called Dollar Cost Ravaging.

What Is Dollar Cost Averaging?

Before we dive into the problem, let’s talk about its positive twin: Dollar Cost Averaging (DCA). This is a strategy you might already know. It’s when you invest a fixed amount of money regularly, no matter what’s happening in the market.

The beauty of DCA is that when prices are high, you buy fewer shares, and when prices drop, you buy more. Over time, this can actually work in your favor, even if the market’s average price doesn’t change.

Here’s a quick example:

| Investment Amount | Share Price | Total Shares Purchased |

| $1,000 | $10.00 | 100 |

| $1,000 | $5.00 | 200 |

| $1,000 | $10.00 | 100 |

| $1,000 | $15.00 | 67 |

| $1,000 | $7.50 | 133 |

| $1,000 | $10.00 | 100 |

If you saved $6,000 over six months, and the share price started and ended at $10, you’d think you would have broken even, right? But you didn’t! You actually bought 700 shares. You exponentially bought more shares in the months the price plummeted. Now your portfolio is worth $7,000 while the price didn’t gain a dime—all thanks to DCA.

That price volatility (those ups and downs in the market) helped you buy more when prices were low. It’s like the old investing mantra: “Buy low, sell high.”

Enter Dollar Cost Ravaging

Now let’s meet DCA’s evil twin: Dollar Cost Ravaging (DCR).

When you take money out of your TSP or any investment, you’re essentially selling shares to generate cash. Think of it like this; you spend your life savings and investing and buying shares. When it’s time to spend the money, you flip it around, turning in your ownership interest (sell) for cash, cash to spend in retirement.

Now to the important point, if you are relying on your TSP to provide supplemental income in addition to your Social Security and FERS Pension (like it was designed to do), you are systematically SELLING shares each month to meet a desired income amount. When the market or investment fluctuates, the number of shares will vary depending on the price.

The opposite of DCA, Dollar Cost Ravaging, will force you to sell exponentially more shares when the investments are down.

Let’s revisit the earlier example, but now assume you’re withdrawing $1,000 per month:

| Withdrawal Amount | Share Price | Shares Sold | Shares Remaining |

| $1,000 | $10.00 | 100 | 400 |

| $1,000 | $5.00 | 200 | 300 |

| $1,000 | $10.00 | 100 | 200 |

| $1,000 | $15.00 | 67 | 133 |

| $1,000 | $7.50 | 133 | 0 |

| $1,000 | $10.00 | 0 | 0 |

In this case, selling more shares when prices were low left fewer shares to grow when the market rebounded. Instead of “buying low,” you’re forced to sell low—and that’s where Dollar Cost Ravaging hurts.

Over the 6-month sample, you only withdrew 5,000 of the original 6,000.

And you didn’t even make it to month 6.

Why the TSP Makes This Worse for Retirees

Here’s the problem: the TSP doesn’t give retirees the flexibility to manage withdrawals effectively.

1. You Can’t Choose What to Sell

Let’s say your TSP is 60% in the C Fund (stocks) and 40% in the G Fund (government securities). Every withdrawal comes out of those funds proportionally—60% from the C Fund and 40% from the G Fund.

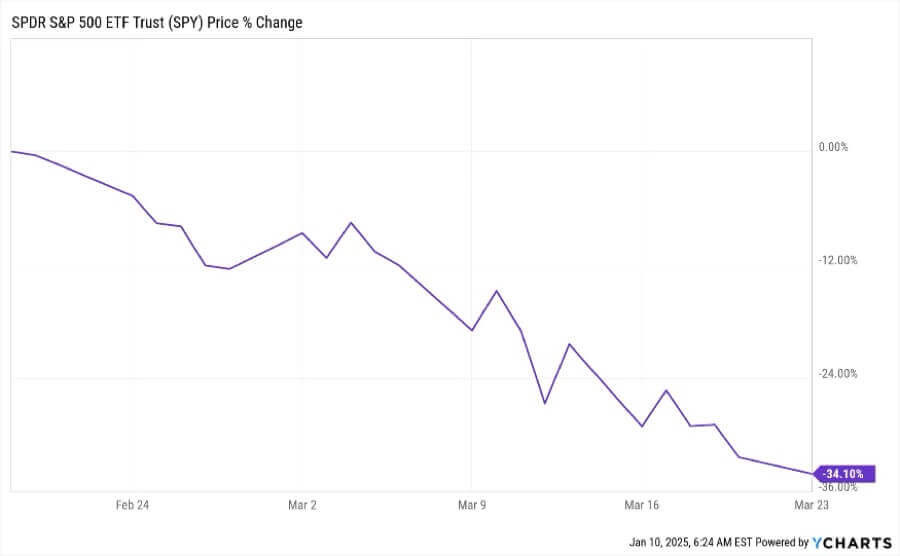

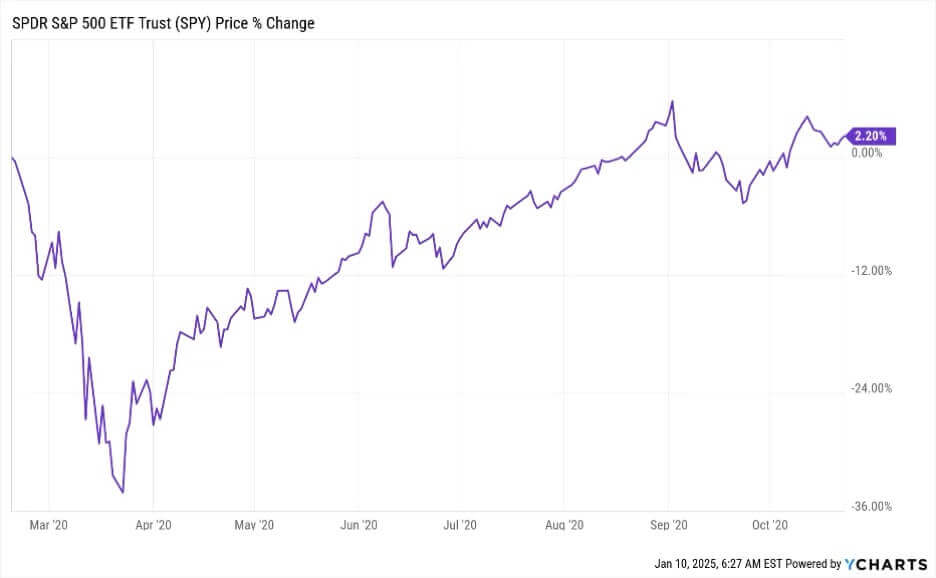

But that’s not ideal. The C Fund is designed to mimic the S&P 500, is meant for growth, and there is much more volatility than the G Fund. Ideally, we are not automatically selling each month out of the C, since it has the largest chance of looking like the chart below.

In the world outside the TSP, during a market downturn, you’d want to pull 100% from the least volatile fund (the G Fund for the TSP) and leave the high growth/high volatile investment like C Fund alone to recover.

2. Mandatory 20% Federal Tax Withholding

By law, the TSP withholds 20% for federal taxes on withdrawals. But what if you don’t need to pay 20% in taxes? For a Married Filing Joint retired couple, earning $150K from their TSP, Social Security and FERS annuity, their total average tax bracket is closer to 11%. While forcing participants to withdraw 20% may eventually result in a tax refund due to this overage, the investment damage is already done. The extra amount withdrawn to accommodate the 20% forces retirees into selling even more shares unnecessarily.

For example, let’s say in my example above, this couple needs $40,000 per year after taxes from their TSP. If they could customize their withdrawal amount to the actual taxes they owe, they would withdraw (and sell funds, remember) about $45,000 per year (not including state taxes).

But because of the 20% withholding rule, they must withdraw/sell $50,000 to hit their $40,000 targets. Given the 60/40 example, that’s an additional forced selling of $3K per year from the C Fund.

Over a 30-year retirement, this adds up. That extra selling, combined with market volatility, can potentially cost you a large chunk due to Dollar Cost Ravaging!

What Can You Do?

Here’s how you can take control:

- Call your congressmen and the TSP and get them to change this rule! But in the meantime, …

- You could Roll Over to a Low-Cost IRA

Move your TSP balance to an IRA with a provider that lets you customize withdrawals. This way, you can choose which funds to sell and avoid dollar cost ravaging. - Once there, Strategically Rebalance

Set up an automatic withdraw from low-volatility funds and replenish them later (rebalance) from higher growth/volatility funds at times of your choosing. (not during at market downturn) - Work with a Tax Advisor and/or Financial Advisor

Calculate your actual tax liability if less than 20% and customize your tax withholding to what you will actually owe to avoid over-withholding and withdrawing more than necessary.

The TSP is fantastic for growing your money, but for retirees, it can leave a lot to be desired. If you’re nearing or in retirement, upgrading to a more flexible plan could make a huge difference—not just for your finances but for your peace of mind.

After all, retirement is about enjoying the fruits of your labor, not worrying about market swings or unnecessary taxes.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC. This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor. This material is for general information only and is not intended to provide specific advice or recommendations for any individual.

There is no assurance that the views or strategies discussed are suitable for all. investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.