If you’ve been watching the news—or just logging into your TSP account—you may be feeling a little uneasy.

Today, April 3, 2025, U.S. stocks dropped more than 1,000 points in a single morning. Why?

According to news outlets… a new round of tariffs, announced by President Trump, reignited fears of a global trade war. Stocks tied to global supply chains—like Apple, Amazon, and Nike—took big hits. Meanwhile, gold shot up, as investors scrambled for “safe” assets.

These kinds of headlines are hard to ignore—especially when your retirement savings are involved. And if you’re like many federal employees, you might be wondering:

- “Should I shift everything into the G Fund?”

- “Will this ruin my chances of retiring on time?”

- “Am I supposed to be doing something right now?”

Let’s slow down, take a breath, and zoom out—way out.

What You’re Feeling Is Normal

When you’re invested in the market—whether it’s your TSP, an IRA, or anything else—volatility is part of the deal. That doesn’t make it fun, but it does make it expected.

And if your instinct is to panic or pull out of your funds when things drop? You’re not crazy. That’s human. In fact, most people react that way when they haven’t been shown what to expect or how their investments behave in different kinds of markets.

That’s why I want to show you something.

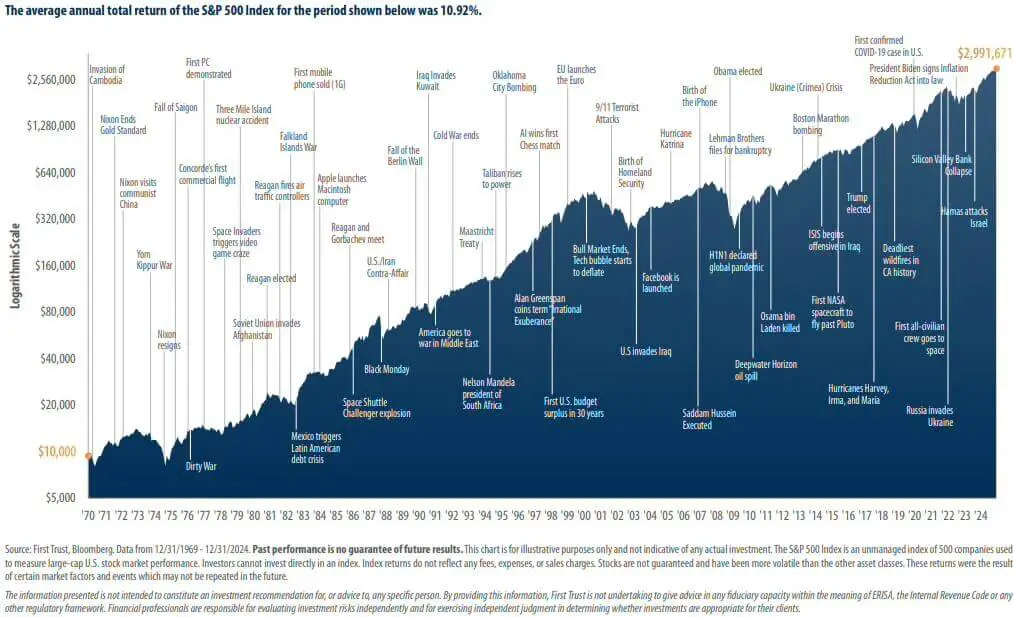

This Chart Tells the Real Story

Take a look at the chart below. It shows the growth of the S&P 500—a broad measure of the U.S. stock market—from 1970 through the end of 2024.

If you had invested $10,000 in 1970 and simply stayed invested, through all the crashes, crises, wars, and downturns, your portfolio would have grown to nearly $3 million by the end of 2024.

But look at all those bumps along the way:

- Nixon resigns (1974)

- Black Monday (1987)

- Dot-com bubble burst (2000–2002)

- 9/11 attacks

- The Great Financial Crisis (2008–2009)

- COVID-19 (2020)

- Russia’s invasion of Ukraine (2022)

- And yes, multiple rounds of trade wars and tariffs, including the one that caused the late-2018 market selloff

Each of these events caused fear, uncertainty, and panic in the moment. But over time, the market recovered—every single time. That’s why this chart is so powerful: it shows that despite how things feel in the moment, history favors long-term investors who stick with their plan.

Been there, Tariff-ed That

This isn’t the first time tariffs have rattled the market. Remember 2018? The fourth quarter saw a nearly 20% market drop, fueled in large part by trade war headlines. Here’s what PBS reported back then:

The Trump administration’s tariffs on imported aluminum, steel, and other goods have introduced a large amount of uncertainty into the global economy. […] The stock market woes come despite signs that the general economy is still doing well.

Sound familiar? Like it could’ve been written yesterday?

That’s the lesson: markets are always digesting uncertainty—whether it’s tariffs, elections, inflation, or even a global pandemic.

And guess what? They’ve historically recovered.

Not a Bug in the System

If you’re a federal employee or retiree, your TSP is likely your largest retirement asset. But here’s what most people don’t realize:

Your TSP investments (namely the C, S, and I) are supposed to go up and down—sometimes dramatically. This is the price you pay for greater growth over safe investments. (Like the G Fund.)

This volatility is a feature of the system, not a bug.

And unless you have a plan in advance built around those swings, it can be very tempting to make poor choices at the worst possible time—like going all in the G Fund and staying there for years as you wait for the best time to back in. I’ve seen that story.

You Don’t Need a Tariff Plan. You Need a Real Plan.

Let’s be honest: You’re not going to build a separate strategy for every potential threat—tariffs, inflation, elections, rising interest rates, cyberattacks, or whatever tomorrow brings.

Instead, what you need is a plan that anticipates those threats. One that:

- Accounts for market volatility

- Fits your time horizon (how close or far you are from retirement)

- Aligns with your risk tolerance and financial goals

- Integrates your other benefits—like FERS, Social Security, Supplement.

- Gives you peace of mind so you don’t have to react to every headline

What Not to Do

Notice I didn’t say jumping in and out of the market. Moving from the C and back into the G Fund and then back to the C Fund. Trust me, I’ve seen how that story ends, and it’s usually not pretty.

More money is lost trying to time the market than is ever gained. Sure, someone in your office, a TSP Facebook group, or the comments section of this blog might brag about nailing the timing, but you rarely hear from the many who tried and failed—and believe me, they far outnumber the lucky few who got it right.

Don’t forget the lessons learned from those TSP millionaires; the real key is staying the course—if you have a plan.

The plan doesn’t have to be complicated. But it does need to be clear—what will you do in market downturns when, not if, they happen.

What You Can Do Now

If you’re unsure whether your TSP is set up correctly—or if you’ve never thought about your comfort zone before—this might be the perfect moment to take a deeper look.

Here’s how you can get started:

- Discover your Tolerance™ – This simple quiz helps you understand your personal tolerance for investment risk.

- Evaluate your TSP allocation – Are you taking too much risk… or too little? Plan in advance.

- Stress-test your retirement plan – How would another 10% market drop affect your future retirement income?

- Get guidance from someone who understands federal benefits – The TSP and Federal Benefits aren’t cookie cutters. They deserve specialized advice.

Final Word: Zoom Out, Stay the Course

The chart says it best: Over time, the market rewards discipline. Every scary moment in history looked like the end of the world when it was happening, but it never was.

So, the next time tariffs make the headlines—or markets drop suddenly—remember this:

- Short-term drops are part of the process.

- Long-term growth rewards those who stay invested.

- Having a plan makes it easier to sleep at night.

Just make sure you have one.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC. Investing involves risks including possible loss of principal. Asset allocation does not ensure a profit or protect against a loss.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries