Another Bill Introduced to Slash Telework for Federal Employees

Another bill has been introduced in the Senate to put limits on federal employees’ use of telework.

Another bill has been introduced in the Senate to put limits on federal employees’ use of telework.

There are three primary types of investment accounts, and different strategies are needed for each to minimize taxes.

FEGLI is not always the best life insurance option for federal employees. These are some important considerations.

The OPM retirement backlog has been on a steady decline so far in 2024.

The go-broke dates for Medicare and Social Security have been pushed back as an improving economy has contributed to changed projected depletion dates according to the latest trustees reports for both programs.

When it comes to annuities, the author says that federal employees can have too much of a good thing.

Required minimum distributions can raise a federal employee’s annual income resulting in higher Medicare premiums.

When is the best day for federal employees to retire? These are some important factors to consider.

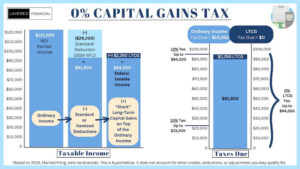

How do capital gains taxes work? Can they ever be avoided entirely?

Federal employees who are planning to work after retirement need to be aware of these potential pitfalls.