The TSP can be a great tool for retired federal employees. But, if not used in the right way, you can quickly lose everything you’ve worked so hard for. In this article, we are going to look at a few ways federal employees can lose money very quickly in the TSP.

100% G Fund?

The G Fund is not a bad fund. But, too much of the G Fund could be a bad thing even in retirement. Retirement can last a very long time and you still want your TSP to grow and keep up with inflation. If you are invested completely in the G Fund and taking TSP withdrawals consistently, your money will get eaten up very quickly.

Investing a portion of your retirement money in investments that offer growth over time is a good way to have your retirement money for your whole life. Yes, the stock market will go down sometimes and that is why it’s helpful to also have a portion of your money in conservative funds.

Sometimes a good rule of thumb is to have 7 years worth of living expenses in conservative funds in retirement and the rest in aggressive funds. As the years go by, try to replace the conservative funds when your aggressive investments are higher.

Another small tip is using the 4% rule. The 4% rule is the percentage of your TSP that you can withdraw annually without losing money over time. So, if you had $1,000,000 in your TSP, you could withdraw $40,000 out of your TSP ($3,333 per month) each year and the odds of you losing money in your retirement is basically 0.

Early Withdrawals

Your TSP is designed to help you have the retirement that you’ve dreamed about but taking money too quickly can destroy its growth over time. I have seen many retirees take large TSP withdrawals early in retirement for large purchases like 2nd homes, boats, etc.

And while there is nothing wrong with using your TSP on the things you want, you need to be careful to understand the ramifications.

Immediately spending a large chunk of your TSP in retirement means there is simply less money there to grow for you over time.

Getting Scared When the Stock Market is Low

Probably the quickest way to lose money in your TSP throughout your career and in retirement is pulling money out of the C, S, & I Funds when the stock market is down. When people notice that their hard-earned money is losing value very quickly, they get scared and decide to invest in something more conservative.

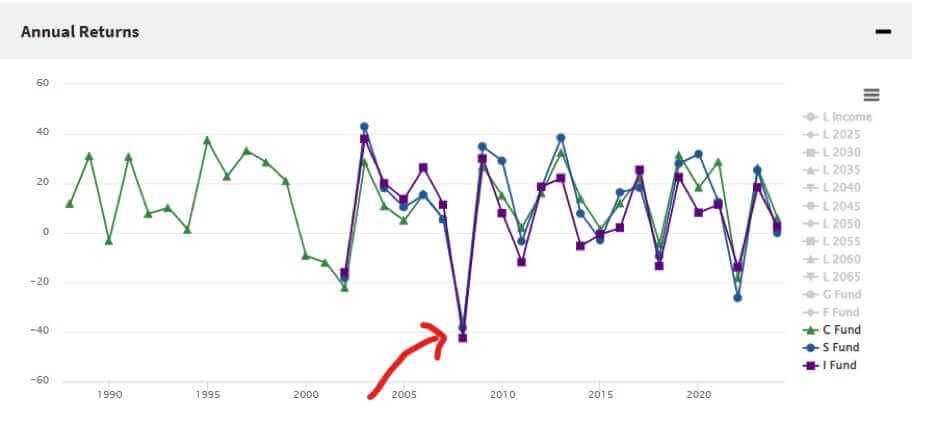

Let’s take a look at what this could look like:

As we can see, there was a time in 2008 that the C, S, & I Funds were down. Many people at that time freaked out and pulled all their money out at the lowest point and started investing in the G and F funds. That is the worst possible time to pull out. They lost about 40% of TSP money.

If people keep switching from aggressive to conservative funds when their returns are low, they will lose money very quickly. It’s important to have hope that things will come back up because throughout history, that’s what it has always done. And just think about it; if the whole stock market is doing badly, you’re not alone.

Conclusion

I hope this was helpful for you to see how you can avoid some pitfalls when it comes to the TSP and investing overall. Remember to think before you make a quick decision. The worst decisions are those made quickly.

Take a moment to evaluate what your goals are in your career or even retirement. Try to make investment decisions that match those goals. Be careful not to change your goals too quickly. Try not to act in fear or spur of the moment.

I wish you good luck investing in TSP. We help a lot of federal employees with the TSP and any other federal employee topic. If you want personalized help, feel free to check out our website, or schedule a one-on-one appointment with us.